Generative Engine Optimization: Analyzing the Capital Flight from Search to Answers

Key Takeaways:

📉 The Short: Traditional SEO tools (Semrush/Ahrefs) are depreciating assets.

📈 The Long: "Answer Infrastructure" (Peec, Profound) is the new Alpha.

💰 The Signal: Peec AI’s $21M Series A proves the "Sovereign Data" model is winning in Europe.

Executive Summary: The Ad-Tech Reset

The digital marketing ecosystem is currently undergoing its most violent structural correction since the introduction of programmatic advertising. For nearly two decades, the "10 Blue Links" model—the foundation of Google's search monopoly and the global SEO industry—served as the primary mechanism for capital allocation in digital discovery. This asset class is now rapidly depreciating. The emergence of Large Language Models (LLMs) and the subsequent integration of "Answer Engines" (ChatGPT, Perplexity, Gemini, Claude) has triggered a capital flight from traditional Search Engine Optimization (SEO) toward a new, volatile, yet highly appreciating asset class: Generative Engine Optimization (GEO).

This report serves as an exhaustive analysis of the nascent GEO sector, validated by the recent financing of Berlin-based Peec AI in November 2025. This transaction is not merely a venture bet; it is a signal of institutional capital acknowledging that the "Zero-Click" future is no longer a theoretical risk but a statistical reality. With zero-click searches exceeding 60% of total volume and organic click-through rates (CTR) for informational queries collapsing by 47% when AI overviews are present, the economic logic of traditional SEO is fracturing.

We posit that capital is moving from optimizing for links—which are functionally depreciating assets in an AI-mediated web—to optimizing for citations and model inference. In this new paradigm, visibility is binary: a brand is either synthesized into the answer or it is invisible. This analysis evaluates the competitive matrix of the GEO sector, focusing on three distinct strategic approaches: the Sovereign Play (Peec AI), the Enterprise Governance Play (Profound), and the Attribution Play (Gauge). Furthermore, we offer a cynical outlook on legacy ad-tech incumbents (Semrush, Ahrefs), predicting that their bolted-on AI features will fail to stem the tide of churn as enterprise budgets shift toward "Answer Optimization" in the 2026 fiscal cycle.

📋 Interactive Tool: The GEO Vulnerability Simulator

Are you exposed to the "Zero-Click" shift? We built a free AI-powered simulator to stress-test specific industries against the new search economy.

👉 Run the Strategic Simulation

1. The Catalyst: Peec AI and the Validation of the Sector

1.1 The Transaction Signal: Deconstructing the $21M Series A

In November 2025, the venture capital landscape received a definitive signal regarding the maturity of the GEO sector. Peec AI, a Berlin-based marketing platform specifically architected for the age of AI search, announced a financing round. This round was led by Singular VC, with participation from a syndicate including Antler, Combination VC, identity.vc, and S20. Following a Seed financing led by 20VC in July 2025, this injection brings Peec AI's total funding to $29 million, marking one of the most significant liquidity events in the nascent GEO sector to date.

The sheer magnitude of this Series A in the current venture climate—characterized by rigorous due diligence and a retreat from speculative tech—underscores the urgency of the problem Peec AI addresses. It validates a specific investment thesis: that the "AI Search Revolution" requires a fundamentally new infrastructure layer, distinct from the tooling of the past decade. While US-centric platforms have largely focused on the technicalities of prompt engineering or the generative capabilities of content creation, Peec AI’s value proposition is rooted in "infrastructure." Specifically, the company has built a proprietary data pipeline that maps source influence, visibility, and sentiment across major AI engines in real-time. This moves the value capture from the application layer (generating text) to the intelligence layer (analyzing how the model thinks).

The timing of this raise is equally critical. Occurring in late 2025, it aligns with a broader market realization that the "experimentation phase" is ending, and the "operationalization phase" is beginning. Enterprises are no longer asking "what is ChatGPT?" but rather "how do we control our brand within it?" Peec AI’s ability to secure this level of funding suggests that they have successfully demonstrated that GEO is not a feature of SEO, but a distinct vertical requiring specialized SaaS solutions.

1.2 The Sovereign Moat: Why Berlin Matters

The geographical location of Peec AI—Berlin, Germany—is a critical differentiator in our investment thesis and a key driver of its valuation. Europe is currently the global epicenter of the data sovereignty movement, driven by the rigorous enforcement of GDPR and the emerging EU AI Act. For American incumbents, GDPR is often viewed as a compliance hurdle or a friction point to be managed. For Peec AI, it is a foundational product feature and a competitive moat.

European brands are currently struggling to maintain visibility across fragmented digital channels—a €2.3 billion addressable market—while simultaneously navigating complex data privacy regulations that reshape how consumer data flows. The concept of "Digital Sovereignty" has moved from policy papers to corporate strategy. Executives are now prioritizing the question of who controls their data and whether foreign governments can access it. This geopolitical anxiety is palpable in boardrooms across the continent, where reliance on US-based tech stacks is increasingly viewed as a strategic vulnerability.

Peec AI’s platform is architected to process multilingual brand data across Europe’s 27 markets while adhering to these strict sovereignty requirements. This creates a defensive moat against Silicon Valley competitors who often struggle to adapt their US-centric, data-hungry models to the European regulatory environment. By positioning itself as the "Sovereign Play," Peec AI secures the patronage of highly regulated European enterprises (finance, automotive, insurance) that are legally inhibited from utilizing non-compliant US tools. The firm’s ability to onboard 1,300+ brands and agencies since its launch in February 2025 suggests that this sovereignty-first approach is finding immediate product-market fit.

Furthermore, the "Sovereign Play" extends beyond mere compliance. It addresses the cultural nuance of the European market. Unlike the homogeneous US market, Europe requires infrastructure that can handle diverse languages, currencies, and consumer behaviors simultaneously. Peec AI's native capability to handle this complexity positions it as the default choice for pan-European conglomerates, effectively blocking US entrants who view Europe as a secondary market.

1.3 The Competitive Context in European Funding

Peec AI's €18 million ($21 million) raise does not exist in a vacuum; it enters a European funding landscape where AI-driven marketing and brand-visibility tools are attracting significant investor attention. The market is witnessing a flurry of activity in adjacent sectors, indicating a broader trend toward AI-native marketing stacks. For instance, France-based Massive Dynamic raised a €3 million pre-Seed round to develop an AI-native marketing-ops suite, while the Netherlands' aizy raised €1.5 million to expand its AI-driven marketing software for SMEs. Additionally, the UK's Plain secured €14.5 million for its collaborative AI-powered support platform.

Germany, however, features strongly in this segment. Berlin-based Talon.One closed a massive €114 million round to scale its AI-enhanced loyalty infrastructure, placing it in the upper tier of funding volumes for the year. With approximately €133 million flowing into comparable or adjacent European startups, Peec AI's raise positions the Berlin-founded company in the mid-scale funding bracket of an increasingly active sector. This context is vital: Peec AI is not an anomaly; it is a leader in a rapidly capitalizing vertical. The density of capital flowing into European AI marketing tools suggests that investors see this region not just as a regulatory fortress, but as a hotbed of innovation in "Responsible AI" and "Sovereign Tech."

1.4 The Founders and the "Precision" Ethos

The leadership team behind Peec AI—Daniel Drabo, Tobias Siwonia, and Marius Meiners—met in Antler's Berlin-based Winter 2024 cohort. This origin story is significant as it highlights the "ecosystem effect" of European tech accelerators in fostering teams that tackle complex, infrastructure-level problems rather than consumer fads.

CEO Marius Meiners has articulated a philosophy of "precision" that permeates the company's product strategy. "We are obsessed with precision. Clean data, clear workflows, and a UI that teams actually love to use," says Meiners. This focus on "craft" and "authenticity" stands in stark contrast to the often chaotic, feature-bloated nature of early AI tools. In a market flooded with "wrapper" startups that simply reskin OpenAI's API, Peec AI's emphasis on proprietary data pipelines and refined user experience (UX) signals a maturity that appeals to enterprise buyers. They are not selling "magic"; they are selling clarity in a complex environment. The platform's ability to map source influence and sentiment in real-time is presented not as a black box, but as a tool for "winning where AI is shaping the narrative". This rhetoric of control and precision resonates deeply with CMOs who feel they have lost control of their brand in the age of generative search.

2. Macro Thesis: The Depreciation of the Click

2.1 The "Great Decoupling" of Search and Traffic

The fundamental driver of the shift to GEO is a phenomenon we term the "Great Decoupling." Historically, search volume and site traffic were positively correlated: as more people searched for information, more people clicked through to publisher websites. This linear relationship underpinned the entire economics of the web, funding journalism, e-commerce, and the open internet. In 2025, this correlation has irrevocably broken.

Data from the first half of 2025 indicates a paradox: while search activity is booming, traffic is collapsing. Daily Google searches have increased by 7-60%, reaching volumes between 9.1 billion and 13.6 billion queries per day. Under the old paradigm, this surge would have resulted in a windfall of traffic for publishers. Instead, the median publisher experienced a 10% year-over-year traffic decline, with non-news content sites down 14% and news publishers down 7%.

This decoupling is driven by the aggressive rollout and user adoption of AI Overviews (formerly SGE). These AI-generated summaries now appear for approximately 13.14% of all queries, a figure that represents a 102% increase from just 6.49% in January 2025. The search engine has evolved from a directory (referring traffic) to a destination (hoarding traffic). The user's intent—to find an answer—is satisfied directly on the Search Engine Results Page (SERP), rendering the click redundant.

Figure 2.1: The Great Decoupling (2024-2025)

Source Data: Digital Bloom 2025 Traffic Crisis Report

2.2 The Zero-Click Epidemic: Statistical Reality

The "Zero-Click" phenomenon is no longer a fringe occurrence; it is the dominant user behavior. Approximately 60% of Google searches now end without a click to a website. This represents a fundamental shift in the utility of the search engine. On mobile devices, where screen real estate is limited and the friction of clicking is higher, the zero-click rate rises to a staggering 77.2%.

This trend is accelerating specifically in high-value verticals. For news-related queries, the proportion of searches ending without a click rose from 56% in 2024 to 69% by May 2025. A Bain & Company study reinforces this, finding that 80% of consumers now rely on zero-click results in at least 40% of their searches. The implication is clear: the majority of users, for a significant portion of their digital lives, are effectively "dark" to traditional web analytics. They are consuming content, forming brand impressions, and making decisions without ever visiting a brand's property.

2.3 The Collapse of Traditional CTR

The introduction of AI Overviews has introduced a massive volatility factor into organic Click-Through Rates (CTR). The presence of an AI Overview is functionally a "tax" on organic traffic. When an AI Overview is present, the CTR for traditional organic results plummets to just 8%, compared to 15% for results without AI summaries—a 47% drop in asset efficiency.

Even more alarming for the legacy SEO industry is the "bleed" effect. Even on queries without AI Overviews, organic CTRs have fallen by 41% year-over-year. This suggests a profound behavioral shift: users are simply clicking less, conditioned by platforms like ChatGPT and Perplexity to expect immediate answers rather than navigation options. The "10 Blue Links" are no longer a utility; they are friction.

The data further reveals that this impact is not evenly distributed. "Informational" queries—the bread and butter of content marketing—are the hardest hit. 88.1% of queries that trigger an AI Overview are informational in nature. This means that the top-of-funnel content that brands use to attract new customers is effectively being demonetized by the search engine itself. Conversely, navigational queries (searching for a specific site) still generate clicks, but the "discovery" layer of the web is being walled off.

2.4 Economic Implications for Enterprise Capital

For the enterprise CFO, this data presents a crisis of capital allocation. Billions of dollars are currently locked in SEO retainers, content production agencies, and technical optimization contracts aimed at ranking for keywords that no longer generate traffic. The "Unit Economics of a Click" have deteriorated to the point of unviability.

As the Zero-Click rate approaches 70% for certain queries, the cost to acquire a visitor via organic search effectively doubles or triples. The volume of addressable traffic shrinks, while competition for the remaining clicks intensifies, driving up the effort required to rank. In financial terms, the "SEO Asset" is depreciating. A ranking of #1 used to guarantee a 30-40% CTR; today, on a SERP with an AI Overview, it might yield less than 10%.

Consequently, capital is fleeing this depreciating asset class. It is moving toward "Model Citations"—the only mechanism to influence the answer that 60-80% of users now consume directly. This is the financial basis for the rise of GEO. It is not just a new marketing tactic; it is a flight to quality, moving budget from an asset that is losing liquidity (links) to one that is gaining it (citations).

2.5 The "Ad-Tech Reset" and the Future of Media M&A

The implications of this shift extend to the macro structure of the media and ad-tech industries. We predict that media and entertainment M&A will top $80 billion as the AI race fuels a higher volume of technology-centric deals. Search's reliance on blue links will fade as AI answers and personalized agents take center stage.

This environment creates a "Reset" where incumbents are vulnerable and new aggregators emerge. Streamers and broadcasters will cross "frenemy" lines, consolidating to survive the battle for attention. In the ad-tech world, this reset means that the tools of the past decade—DMPs, cookie-based attribution, and keyword trackers—are obsolete. The new stack will be built around LLM analytics, sovereign data pools, and agent-based attribution.

3. The New Asset Class: Model Citations and Answer Optimization

3.1 Defining the Asset: The Model Citation

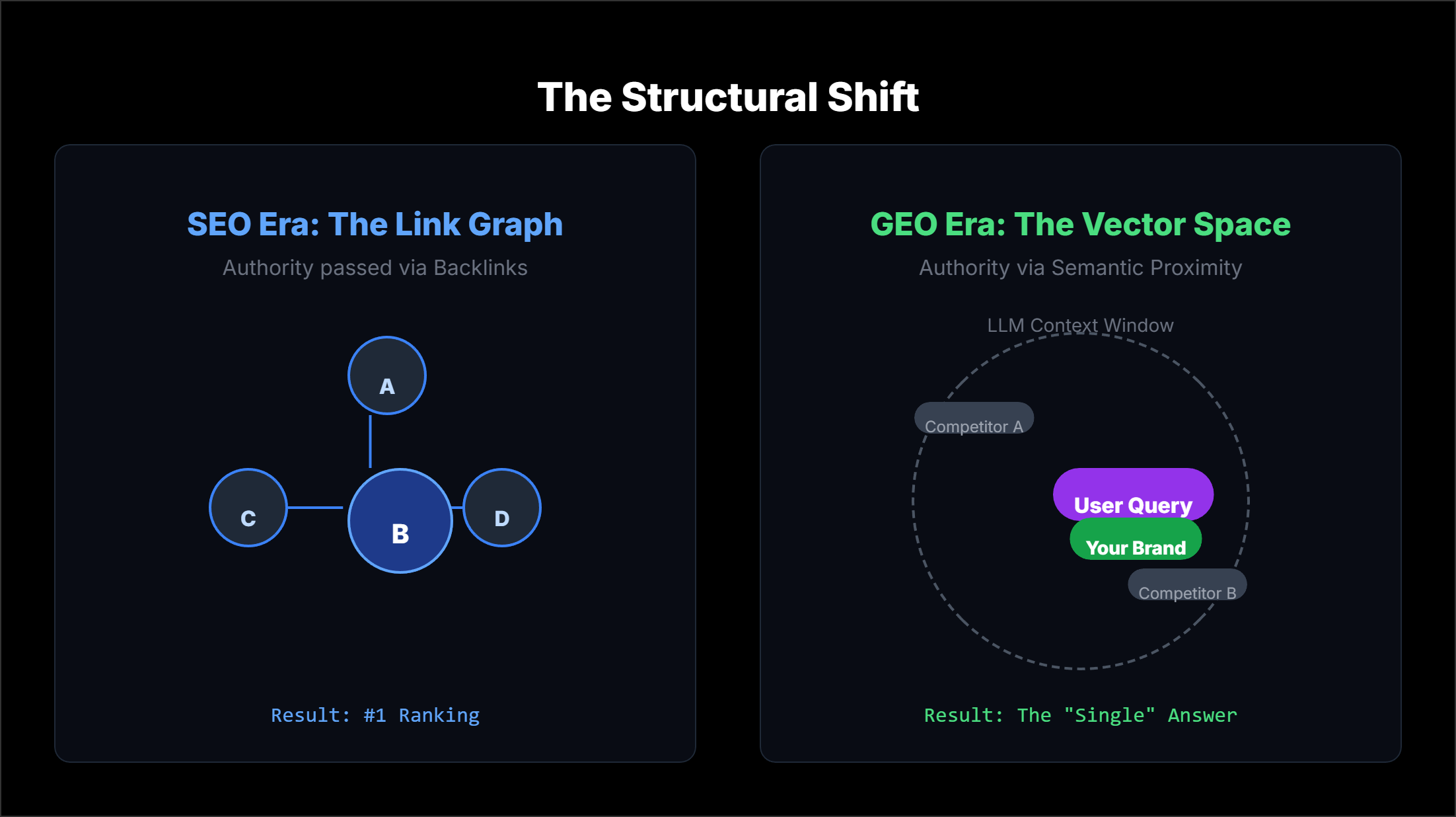

In the SEO era, the primary digital asset was the "Backlink"—a hyperlink from one site to another, acting as a vote of confidence that search algorithms (like PageRank) could count. In the GEO era, the primary asset is the "Model Citation" or "Vector Inclusion."

A Model Citation occurs when a Large Language Model (LLM) retrieves information from a specific entity and synthesizes it into a generated response. Unlike a backlink, which transfers authority via a graph structure, a citation validates relevance, factual accuracy, and contextual appropriateness within the model's latent space. It is a probabilistic event, not a static link.

This asset is far more complex than a link. It involves the model "understanding" the brand entity. For example, does the model associate "Peec AI" with "Data Sovereignty" and "Berlin"? If so, when a user asks about "GDPR-compliant marketing tools," the model will probabilistically generate Peec AI as part of the answer. Optimizing for this requires teaching the model, not just gaming the algorithm.

Figure 3.1: Structural Shift from Web 2.0 to Web 3.0

Asset: The Link Asset: Vector Citation

3.2 The Mechanics of Appreciation: From Keywords to Entities

Optimizing for this asset requires a fundamentally different technical approach, often referred to as "Answer Engine Optimization" (AEO) or GEO. The shift is from "Keywords" to "Entities."

Entity-First Indexing: Traditional SEO focused on matching keywords in headers and metadata. GEO focuses on entity mapping. AI search engines are trained to respond to the entirety of a user's question, understanding the relationships between concepts. Brands must own topics comprehensively, connecting subtopics to build "Topical Authority" that the model recognizes. This means creating content clusters that define the brand's expertise in a way that is "machine-legible."

The "Winner-Take-All" Dynamic: Success in AI search is binary. In a list of 10 blue links, being #4 was still valuable. In an AI answer, the model might only cite 1-3 sources. "Either you're listed in the answer or you're totally invisible". This creates a power law distribution where the top entity captures almost all the value (visibility), and the long tail gets nothing.

The Sovereignty of Sentiment: In traditional search, a negative review might rank #4, and a user might skip it. In AI search, a negative sentiment is synthesized into the primary answer. "The customer support was terrible" becomes a defining attribute of the brand entity within the model. Therefore, Reputation Management becomes inextricably linked to GEO. You cannot optimize for visibility without optimizing for sentiment; they are the same variable in the model's calculation.

3.3 The Shift to Zero-Click Revenue: Measuring the Unmeasurable

The ultimate metric for this new asset class is not traffic, but "Leads from AI Search" or "Zero-Click Revenue." This involves a sophisticated approach to measurement that moves beyond the server log.

The value is captured in the mind of the user, not the log of the server. A user sees the brand in a ChatGPT answer, trusts the synthesis, and then later navigates directly to the site to convert. Traditional attribution would call this "Direct Traffic." GEO attribution calls this "AI-Influenced Revenue."

To measure this, forward-thinking companies are implementing:

Zero-Party Data Collection: Adding "How did you hear about us?" fields with options like "ChatGPT," "Perplexity," or "AI Search".

Correlative Uplift Analysis: Measuring the correlation between "Share of Voice" in AI answers and the uplift in direct traffic or branded search volume.

Agent Analytics: Analyzing server logs to see when AI crawlers (like GPTBot) are accessing content, using this as a proxy for "indexing" by the model.

3.4 The Content Shift: "Machine-Legible" Strategy

To win these citations, content strategy must evolve. The "Humanized Content" paradox is emerging. While AI rewards "authenticity" and "firsthand experience" (E-E-A-T), the structure of the content must be optimized for machine ingestion.

This means:

Direct Answers: Providing succinct, direct responses to common queries within the first 150 words of a page.

Structured Data: Heavy use of Schema markup to help the AI parse entities and relationships.

Quoted Statistics: Providing unique, quotable data points that the AI can extract as "facts" to support its generated narrative.

Conversational Tone: Writing in a natural, conversational style that mirrors the way users prompt the model, increasing the probability of a match.

The goal is to be the "source of truth" that the model relies on. This requires a shift from "content farms" (mass-producing generic articles) to "insight engines" (producing unique, high-value data and perspectives).

4. Competitive Matrix: The Battle for the GEO Stack

The market for GEO tools is rapidly segmenting based on the specific anxieties of the buyer. We identify three primary categories: Sovereignty (Peec AI), Governance (Profound), and Attribution (Gauge).

4.1 Peec AI: The Sovereign / GDPR Play

Core Value Prop: "Help marketers win where AI is shaping the narrative, without adding complexity".

Target Persona: European CMOs, Data Privacy Officers, Regulated Industries (EU).

Key Differentiation:

Data Sovereignty: Built-in compliance with EU regulations, handling data within local jurisdictions. This is the critical wedge in the European market.

Berlin-Native: Culturally and technically aligned with the fragmented European market (multilingual, multi-jurisdictional).

Simplicity: Focuses on "clean data, clear workflows" rather than overwhelming technical complexity.

Investment Verdict: Peec AI is the defensive play. As data nationalism rises, European enterprises will be forced to decouple from US-based analytics tools that cannot guarantee sovereignty. Peec AI captures this regulatory churn. Their ability to process 27 markets simultaneously gives them a scale advantage in Europe that is hard to replicate.

4.2 Profound: The Enterprise Governance / Brand Safety Play

Core Value Prop: "AI Without Blind Spots." The complete platform to understand and control AI presence.

Target Persona: Fortune 500, Healthcare (HIPAA), Finance, Legal.

Key Differentiation:

Governance & Compliance: SOC 2 Type II compliant, HIPAA compliant. This is the "Enterprise Grade" stamp required by procurement departments.

Brand Safety: Focuses on "Sentiment Analysis" and "Hallucination Monitoring." It tracks how the AI portrays the brand, not just if it mentions it.

Shopping Analysis: Specifically analyzes product positioning in ChatGPT Shopping, a critical feature for e-commerce enterprises.

Three Data Vectors: Prompts/Responses, Agent Analytics (Server logs via CDN integration), and Real User Conversations (Panel data). This multi-vector approach provides a triangulation of truth that single-vector tools lack.

Investment Verdict: Profound is the insurance play. Large enterprises are terrified of AI "hallucinations" damaging their brand. Profound sells the dashboard that monitors this risk. Raising over $58 million positions them as the best-capitalized player for the high end of the market. They are effectively the "DoubleVerify" of the AI age.

4.3 Gauge: The ROI / Attribution Play

Core Value Prop: "Gap Analysis" and measuring the unmeasurable.

Target Persona: Performance Marketers, Growth Hackers, ROI-focused CMOs.

Key Differentiation:

Gap Analysis: Specifically identifies prompts where competitors appear, and the user does not. This is a direct tactical tool for gaining market share.

Attribution Focus: While technical details are proprietary, Gauge markets itself on the ability to track "Leads from AI Search" and connect GEO efforts to downstream revenue.

Actionable Recommendations: Moves beyond monitoring to specific content actions to close visibility gaps.

Investment Verdict: Gauge is the offensive play. It appeals to marketers who need to justify their budget with hard metrics. In a recessionary environment, the tool that proves ROI wins. While they may lack the enterprise compliance moat of Profound, their focus on "making money" resonates with the mid-market.

4.4 Comparative Matrix

5. The Innovator’s Dilemma: The Obsolescence of Legacy Ad-Tech

5.1 The "Bolted-On" Fallacy: Incumbents in Denial

The incumbents of the SEO era—Semrush and Ahrefs—are currently engaged in a desperate attempt to retrofit their platforms for the AI age. Our analysis suggests this will fail. The innovator's dilemma is in full effect: these companies are beholden to their existing revenue streams (keyword tracking) and cannot fully pivot to the new paradigm (entity tracking) without cannibalizing their core business.

The criticism from the market is sharp and consistent: AI features in these tools feel "bolted on" rather than native. Users report that "AI overview widgets in the usual SEO tools feel like they're bolted on," and are turning to dedicated tools like Profound and newer entrants for genuine insight. The "feature" vs. "platform" debate is settled; users view GEO as a platform-level shift, not a feature-level addition.

5.2 The Ahrefs Denial: A Defensive Stance

Ahrefs, in particular, displays the classic symptoms of incumbent inertia. Their public messaging—"AI can't replace SEO tools"—is a defensive stance aimed at protecting their subscription base. While they have introduced "Brand Radar" to track mentions, their core business model relies on the tracking of hyperlinks and keyword volume.

In a GEO world, keyword volume is a metric of declining relevance. "Prompt Volume"—the number of times a concept is queried in natural language—is the new currency. Legacy tools do not have access to the "firehose" of prompt data that LLM-native partnerships or panel-based tools (like Profound's panel) possess. Ahrefs is optimizing for a query syntax ("best running shoes") that is being replaced by conversational complexity ("I'm training for a marathon in rainy conditions, what shoes should I buy?").

5.3 The Data Disconnect: Blind Spots in the Console

Legacy tools are increasingly blind to the new reality. Google Search Console data—the lifeblood of SEO tools—is becoming "patchy," with historical trend data truncated or incomplete due to the shift to AI responses. "Marketers... are now grappling with incomplete datasets, forcing a scramble toward answer engine optimization... as traditional clicks evaporate".

Semrush and Ahrefs are built on the architecture of the "Click." They track rankings to predict clicks. When the click disappears (Zero-Click), their predictive models break. They are selling maps for a territory that no longer exists. If a tool cannot tell you how your brand appears in a zero-click result, it provides zero value for 60% of searches.

5.4 The Vulnerability of the SMB

While Profound attacks the enterprise, and Peec AI locks down Europe, the SMB market—Semrush's stronghold—is vulnerable. SMBs are the first to cancel subscriptions when ROI becomes opaque. As organic traffic drops, the $129/month subscription to an SEO tool that tracks "10 blue links" becomes hard to justify. We predict a significant churn event for Semrush in late 2026 as SMBs realize that "ranking #1" no longer guarantees customers. The commoditization of "basic SEO" by AI agents (who can do keyword research automatically) further erodes the value of these tools.

6. Outlook: The 2026 Budget Shift and the "Ad-Tech Reset"

6.1 The Agency Crisis: Adapt or Die

The agency model is facing an existential threat. "By the end of 2026, marketing agencies will be materially changed". The low-margin, project-based SEO retainer is dead. Agencies that sell "10 blog posts a month" or "link building" will see their contracts cancelled as clients demand "Answer Optimization."

We predict a massive consolidation. "A dentsu or WPP acquisition will trigger a wave of agency reviews". Large holding companies will acquire specialized GEO agencies (or tool-native agencies) to replace their dying SEO divisions. The agency of 2026 will not be an "agent" but a "purveyor of enterprise platforms", reselling access to tools like Profound and Peec AI. The service layer will thin out, and the software layer will thicken.

6.2 The Rise of "Answer Optimization" Budgets

By 2026, we forecast a formal bifurcation in marketing budgets.

Old Bucket: SEO / Content Marketing (Depreciating).

New Bucket: Answer Optimization / Brand Sovereignty (Appreciating).

CMOs will face the "AI Accountability Mandate". They will need to report on how the brand is perceived by AI agents. "The competitive advantage won't be who uses AI, but who trains, governs, and trusts it responsibly".

This shift will drive capital toward platforms that offer Governance (Profound) and Sovereignty (Peec AI). The "wild west" of generative AI will end, replaced by a disciplined, regulated, and measured approach to managing the brand entity within the machine. Just as "Brand Safety" became a line item in programmatic, "Model Safety" will become a line item in GEO.

6.3 Strategic Prediction: The Agentic Web

Looking further ahead, the consumer is disappearing from the loop entirely. "AI agents will fundamentally alter how brands reach consumers... 24% of AI users already employ AI shopping assistants".

In this Agentic Economy, marketing is no longer about capturing human attention; it is about "predisposing autonomous agents that execute transactions". Brands must produce "machine-legible content" structured for the agent, not the human eye.

This is the final nail in the coffin for the "10 Blue Links." Agents do not click links; they ingest data. The winners of this cycle—Peec AI, Profound, and Gauge—are building the infrastructure for this machine-to-machine commerce. The losers—Semrush, Ahrefs, and traditional publishers—are optimizing for a human browser that is slowly going extinct.

6.4 The "Ad-Tech Reset"

This entire shift represents a "Reset" of the ad-tech stack. We are moving from a probabilistic model based on cookies and clicks to a deterministic model based on citations and agent actions. The companies that build the "truth layer" for these agents—verifying that the data they ingest is accurate and safe—will become the new giants of the industry. Peec AI's Series A is the first major bet on this future, but it will not be the last.

Conclusion

The Series A financing of Peec AI is the bellwether for a broader rotation of capital. We are witnessing the end of the "Search" era and the beginning of the "Answer" era. The value of the traditional search index is collapsing under the weight of zero-click behaviors, while the value of the "Model Citation" is appreciating rapidly.

Investors should look for "Sovereign" and "Governance" plays that offer defensive moats against the chaotic nature of LLMs. We are short legacy SEO tools that fail to decouple their value proposition from the click, and we are long the infrastructure layer of the new Agentic Web. The flight from search to answers is not a trend; it is a permanent structural migration of digital value. The question for the enterprise is no longer "where do I rank?" but "who controls the answer?"

What's Next? Don't guess your exposure. We have modeled the vulnerability of 12 major industries against this shift.

To filter through the noise view the complete feed of funding rounds at Roundly.io

Check out my other blog posts:

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 17

Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

Nov 15

Top AI Investors 2025 YTD by Dollars and Deal Count

Nov 14

AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market