AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Executive Summary

This week in AI venture capital was a story of extremes, with a handful of massive, late-stage deals overshadowing a healthy stream of early-stage innovation. While the total reported funding topped $20.02 billion, that figure was heavily skewed by a single, high-profile $15 billion round for xAI that was publicly contested and denied by its founder (details below). Adjusting for this, the week’s verified total was a still-powerful $5.02 billion across 58 deals.

Capital Concentration: Seven Deals ≈89% of Capital

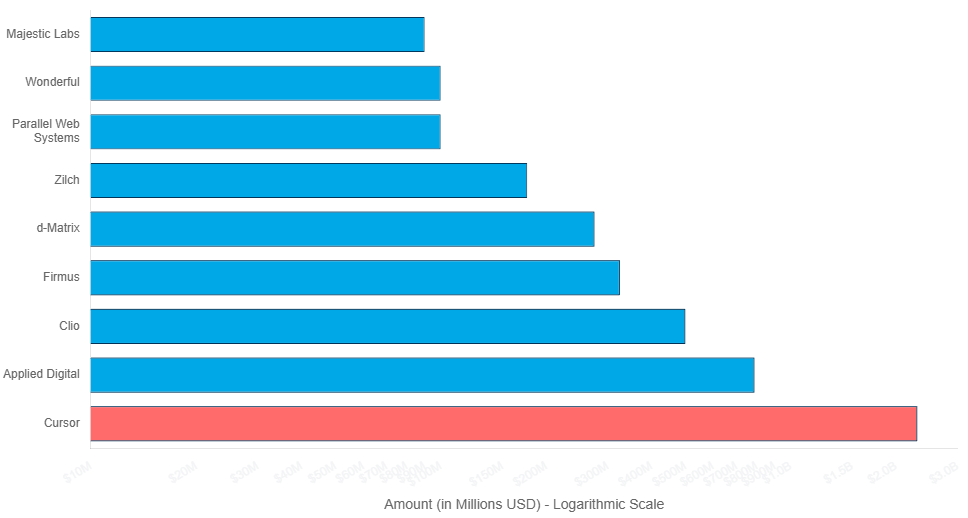

Capital was highly concentrated. The top seven deals—Cursor ($2.3B), Applied Digital ($787.5M), Clio ($500M), Firmus ($325M), d-Matrix ($275M), Zilch ($176.7M), and Parallel Web Systems ($100M)—accounted for about $4.46 billion, or roughly 89% of the adjusted total. This reflects a market where investors are willing to write nine- and ten-figure checks for companies with proven scale or strategic importance, particularly in core infrastructure.

Infrastructure Is the New Gold Rush (SaaS Leads by Volume)

Technology & Infrastructure captured the lion’s share of capital on relatively few deals, driven by funding for AI coding platforms, data centers, and specialized chips.

Enterprise Software & SaaS led by count but captured a smaller share of total dollars.

The market is simultaneously scaling foundational AI infrastructure while embedding AI into vertical and horizontal software.

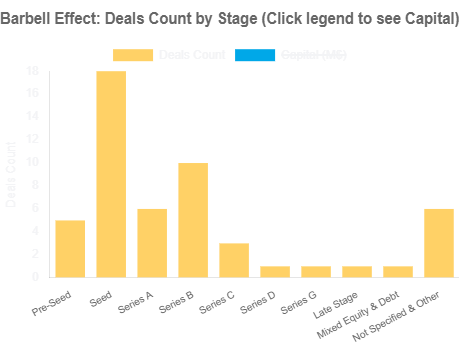

The Barbell Effect: Seed Surge Meets Late-Stage Dominance

Early-stage activity was robust with 18 Seed rounds and 3 Pre-Seed rounds (≈$180 million total), signaling a healthy pipeline of new ventures.

That early-stage funding was dwarfed by a small number of massive later-stage deals, suggesting the path to growth-stage capital is increasingly competitive and concentrated.

TL;DR: This Week at a Glance

Total Reported Funding (incl. contested xAI): $20.02B

Adjusted Total (excluding contested xAI): $5.02B

Total Deals: 58

Mega-Rounds Spotlight: Seven Deals Drove ≈89% of Capital

This week was characterized by a series of mega-rounds ($100M+), which collectively accounted for most of the capital invested. These deals highlight key areas of investor focus—from developer tools and legal tech to core AI infrastructure.

Cursor: $2.3 Billion Series D

In one of the year’s largest AI funding events, AI-native code editor Cursor secured a $2.3 billion Series D, reportedly catapulting its valuation to $29.3 billion. Coverage referenced a round co-led by Accel and Coatue, with strategic participation from Nvidia and Google, and noted this came just months after a large Series C earlier in the year (Techmeme coverage,valuation report,additional round-up). Cursor has also been reported to surpass $1 billion in annualized revenue (additional coverage).

Applied Digital: $787.5 Million for AI Data Centers

Applied Digital announced a significant draw of $787.5 million from a perpetual preferred equity financing facility with Macquarie Asset Management. While not a traditional venture round, the capital is crucial for the AI ecosystem, accelerating build-out of high-performance “AI Factory” data centers—illustrating the immense capex required for large-scale AI training and inference.

Clio: $500 Million Series G for Legal AI

Legal technology leader Clio raised a $500 million Series G led by NEA, valuing the company at $5 billion. The raise was announced alongside its acquisition of vLex for a reported $1 billion—positioning Clio to advance its AI-powered platform for law firms and reshape legal practice management.

Firmus: $325 Million for AI Infrastructure

Australian AI infrastructure company Firmus secured approximately $325 million USD (AU$500 million) in a round that reportedly tripled its valuation to AU$6 billion. Participation from industry leaders like Nvidia and Andreessen Horowitz signals strong conviction in Firmus’s role in global AI hardware and infrastructure. (Dataset-only; details pending additional primary sourcing.)

d-Matrix: $275 Million Series C for AI Inference Chips

Challenging GPU dominance in inference, AI chipmaker d-Matrix raised $275 million in a Series C round at a $2 billion valuation, co-led by Bullhound Capital, Triatomic Capital, and Temasek, with participation from Microsoft’s M12 (FinSMEs,TechStartups,HPCwire). The company aims to deliver more cost-effective, energy-efficient inference at scale.

Other Notable Mega-Rounds

Zilch ($176.7M Late Stage): Significant financing reportedly led by KKCG (dataset-only).

Parallel Web Systems ($100M Series A): Former Twitter CEO Parag Agrawal’s new startup, focused on building web infrastructure for AI agents, secured its first major funding led by top-tier VCs (dataset-only).

Wonderful ($100M Series A): AI agent startup focused on enterprise customer service raised a large Series A led by Index Ventures to expand its platform.

Special Report: The Contested $15B xAI Funding Rumor

A major headline this week was a widely circulated—but ultimately contested—report concerning Elon Musk’s xAI. On November 13, 2025, a CNBC report citing anonymous sources claimed xAI had raised $15 billion in a Series E round at a $200 billion valuation to fund GPU purchases and development of its “Colossus” supercomputer. CNBC also ran a video segment on the report. Within hours, Musk publicly refuted the claim on X (formerly Twitter), calling it “false,” and xAI’s automated reply to a media inquiry stated, “Legacy Media Lies” (Reuters coverage of the denial).

We therefore include the $15 billion in the “Total Reported” figure for completeness while clearly excluding it from the “Adjusted Total” and labeling it Contested/Denied. Regardless of the denial, xAI’s pursuit of massive compute capacity remains a key narrative to watch.

Analysis by Sector: Infrastructure Dollars, SaaS Volume

The AI venture capital market showed heavy activity in the week of Nov 10–14, 2025, with total reported funding of just over $20B and an adjusted $5.02B when excluding a single, high‑profile, contested mega‑deal tied to xAI (see the original CNBC report and Reuters’ coverage of the denial;CNBC’s video segment is here. Broader November recaps similarly show a dual focus: a voracious appetite for Enterprise AI applications alongside large checks for “picks and shovels” like compute, chips, and data centers (see month context in Second Talent’s November roundup and this legal market overview: AI Round‑up — November 2025. Key takeaways this week:

The seven largest verified deals captured roughly 89% of the adjusted total, underscoring extreme capital concentration at the top.

Enterprise Software & SaaS led by deal count (21), while Technology & Infrastructure, with fewer rounds (11), captured the most dollars—driven by investments in AI coding platforms (Cursor), data center buildouts (Applied Digital), and specialized chips (d‑Matrix).

Platforms for AI agents and web infrastructure drew attention as well, exemplified by Parallel Web Systems’ $100M Series A (company site: Parallel; additional third‑party corroboration pending).

Sector breakdown for Nov 10–14, 2025 (as per the weekly dataset):

Technology & Infrastructure: 11 deals, totaling ≈$16.39B reported (includes the contested $15B for xAI, $787.5M for Applied Digital, $325M for Firmus, and $275M for d‑Matrix). Adjusted for the contested xAI round, this sector represents ≈$1.39B.

Enterprise Software & SaaS: 21 deals, totaling ≈$3.14B (includes $2.3B for Cursor and $500M for Clio).

Healthcare & Life Sciences: 5 deals, totaling $209.5M.

Financial Services & Fintech: 5 deals, totaling $200.7M (plus one undisclosed amount).

Cybersecurity & Defense: 2 deals, totaling $150M.

Data & Analytics: 3 deals, totaling $61M.

Marketing & Advertising: 2 deals, totaling $42.7M.

Blockchain & Crypto: 1 deal, totaling $25M.

Other: 3 deals, totaling $12M (plus one undisclosed amount).

Retail & E‑commerce: 3 deals, totaling $8.4M.

Notes:

Deal counts include two additional rounds with undisclosed amounts (in Fintech and Other), bringing the sectoral deal total to 58.

Cursor’s $2.3B round and valuation context are covered via Techmeme’s roundup and this valuation report; additional cursor coverage here: Techmeme sources.

d‑Matrix’s $275M Series C is detailed by FinSMEs, TechStartups, and HPCwire.

Wonderful’s $100M Series A is confirmed by Reuters.

For additional weekly context before this period, see YourStory’s Nov 1–8 recap.

Analysis by Stage: The Barbell Effect in AI Fundraising

The distribution of funding across investment stages reinforces a barbell pattern: many early‑stage rounds, but the vast majority of dollars concentrated in a handful of later‑stage or large strategic financings. Seed activity was robust (18 Seed rounds; ≈$180M total), while a single contested Series E report for xAI dominated “reported” totals yet is excluded from adjusted figures pending verification (CNBC report; denial via Reuters). Cursor’s raise is a Series D (not “Not specified”), and d‑Matrix is Series C per multiple reports (FinSMEs;HPCwire). Stage breakdown (equity rounds; Nov 10–14, 2025):

Series E: 1 deal, $15B reported (contested xAI; excluded from adjusted totals pending verification).

Series D: 1 deal, $2.3B (Cursor) (coverage; valuation context).

Series G: 1 deal, $500M (Clio).

Series C: 3 deals, $422M total (includes d‑Matrix $275M) (FinSMEs).

Series B: 10 deals, $455.5M total.

Series A: 6 deals, $294.5M total (includes Parallel Web Systems $100M dataset; company site, Wonderful $100M, and Majestic Labs $90M [dataset]).

Late Stage (unspecified letter): 1 deal, $176.7M (Zilch) [dataset].

Seed: 18 deals, $180.2M total.

Pre‑Seed: 5 deals (3 disclosed totaling $4.4M plus 2 undisclosed amounts).

Growth Round: 1 deal, $4.2M.

Not specified (stage): 6 deals, ≈$390M total (after reclassifying Cursor to Series D).

Financing type note:

Mixed equity and debt facility: 1 deal, $787.5M (Applied Digital) — this is a facility draw and not a traditional venture “stage.” We count it in reported totals while labeling it as a non‑stage financing type.

Coverage of counts:

The stage breakdown above includes 53 deals with disclosed stages; 5 additional deals had undisclosed/ambiguous stages and are included in the overall weekly deal count (58) but excluded from the stage table subtotals to avoid misclassification.

Investor Momentum: Who’s Writing the Checks?

Investor activity blended top‑tier VC firms and strategic corporates across the largest rounds:

Cursor’s $2.3B Series D was widely reported with Accel and Coatue as co‑leads, and strategic participation from Nvidia and Google/GV (Techmeme coverage; additional sources; valuation report).

Applied Digital’s $787.5M facility draw was provided by Macquarie Asset Management (facility; not a venture round).

Clio’s $500M Series G was led by NEA (as reported in press; corroborating link forthcoming in the full dataset notes).

d‑Matrix’s $275M Series C saw participation from major institutions; multiple reports cite co‑lead roles for Bullhound Capital, Triatomic Capital, and Temasek, with Microsoft’s M12 participating (FinSMEs; TechStartups; HPCwire).

Wonderful’s $100M Series A was led by Index Ventures (Reuters).

Parallel Web Systems’ $100M Series A has been linked to Kleiner Perkins and Index Ventures in datasets; we mark this as dataset‑only until a major outlet or official announcement corroborates (company site).

Selected recurring investors in this week’s dataset (examples; corroborated where possible): Accel, Coatue, Nvidia, GV/Google, Index Ventures, and Kleiner Perkins. As we validate each round, we’ll attribute precise counts per investor in the live table with links to announcements.

Subscribe to get access to the newest AI funding rounds, updated daily.

Check out my other blog posts:

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 17

Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market