Top 20 VCs Investing in AI in 2025 (The Active List)

Executive Summary: The Great Decoupling and the Hardening of Intelligence

By the close of 2025, the global venture capital ecosystem has undergone a structural metamorphosis so profound that the metrics of previous years—deal count, unicorn births, and sheer fundraising volume—no longer serve as adequate barometers for market health. The "AI Hype Cycle" of 2023 and 2024, characterized by the indiscriminate funding of foundational model wrappers and speculative generative interfaces, has not merely subsided; it has been aggressively culled. In its wake, a disciplined, high-stakes environment has emerged, defined by a phenomenon we designate as the "Great Decoupling."

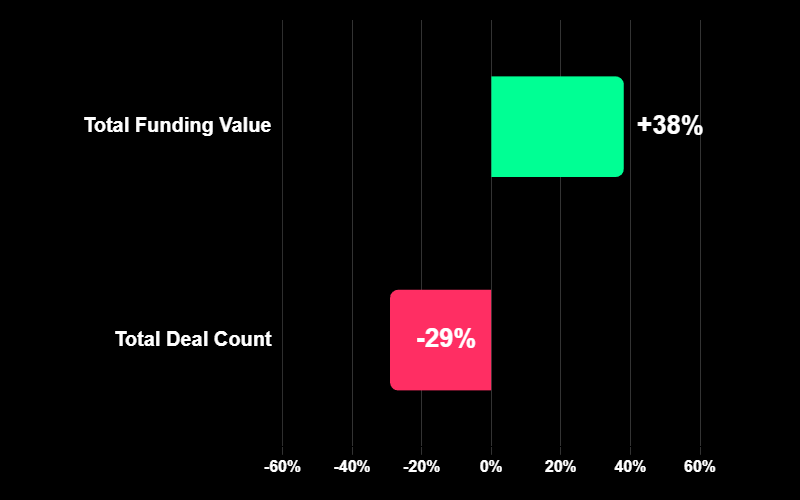

The "Great Decoupling" (Year-Over-Year)

Capital is concentrating (Funding Up), but fewer deals are happening (Volume Down).

This decoupling refers to the extreme bifurcation of capital allocation. On one side lies the "Infrastructure Industrial Complex"—a capital-intensive war zone where sovereign-scale investments are required to train frontier models and build the physical data centers to house them. On the other side lies the "Application Renaissance," a burgeoning but highly selective market for vertical-specific agents that replace human labor rather than merely augmenting it. The middle ground—generic SaaS and thin innovation layers—has become a capital wasteland.

Data from the third quarter of 2025 illuminates this new reality with stark clarity. Global venture funding has surged to $97 billion, marking a 38% increase year-over-year. However, this topline growth masks the underlying concentration: nearly 30% of all capital deployed in Q3 2025 went to just 18 companies raising "megarounds" of $500 million or more. The drivers of this surge are not distributed software bets but massive capital expenditures into the "Infrastructure Giants"—companies like Anthropic ($13 billion raised), xAI ($5.3 billion), and Mistral ($2 billion).

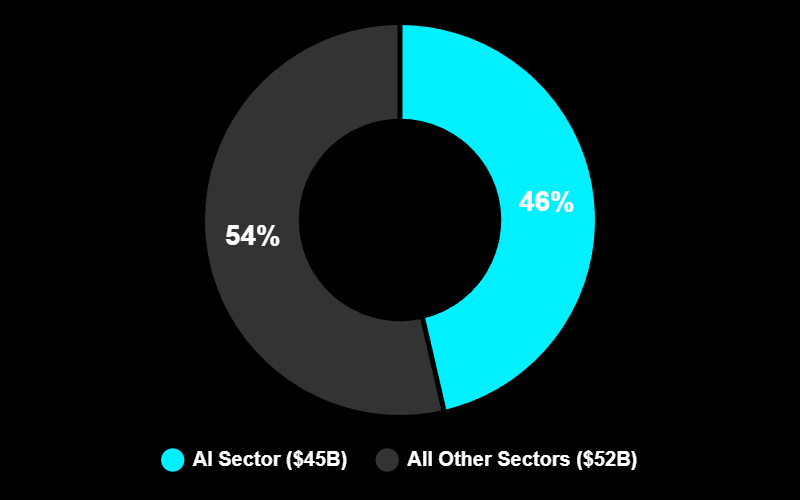

Global Venture Allocation (Q3 2025)

AI has effectively consumed nearly half the asset class ($45B of $97B).

The narrative of 2025 is no longer about "discovery" but "deployment." The cost of entry has skyrocketed, and the "Red Flags" for investors have shifted from technical feasibility to legal defensibility and copyright litigation. As the market stabilizes, the distinction between "software" and "AI" is vanishing—in 2025, all investable software is presumed to be intelligent, and the premium is paid only for systems that possess agency.

This report serves as an exhaustive strategic analysis of the Top 20 Venture Capital firms defining this era. These firms have been selected based on their Q3/Q4 2025 activity, the clarity of their investment theses, and their ability to navigate the technical and legal complexities of the modern AI stack.

The 2025 Macro-Capital Landscape

The following data synthesizes the current state of capital distribution as of late 2025, highlighting the concentration of resources that defines the current investment climate.

At a Glance: The 2025 AI Investment Landscape

Total Q3 Funding: $97 Billion (+38% YoY)

Top Sector: AI Infrastructure (46% of capital)

Biggest Trend: The "Great Decoupling" between Infra and Agents.

Top Active VCs: a16z, Sequoia, Lightspeed, Menlo.

Part I: The Infrastructure Giants (The Kingmakers)

The first category of investors represents the "Kingmakers." These firms operate with assets under management (AUM) that rival small nation-states. Their investment thesis in 2025 has evolved from simply funding Large Language Models (LLMs) to funding the entire "industrial supply chain" required to sustain them—from nuclear energy and specialized silicon to the data orchestration layers that feed the beasts. They believe that intelligence is the new oil, and they are buying the refineries.

1. Andreessen Horowitz (a16z)

2025 Investment Thesis: "The Industrialization of Intelligence and the Prosumer Revolution." a16z is betting that AI is a heavy industry requiring massive capital expenditure in physical and digital infrastructure, coupled with a belief that the "Application Layer" will be driven by startup adoption before enterprise standardization.

Strategic Analysis: Andreessen Horowitz remains the heavyweight champion of the AI ecosystem, leveraging a strategy often described as providing "Oxygen" to the market. In 2025, this means ensuring their portfolio companies have preferential access to the scarcest resource in the digital economy: compute. By securing massive allocations of GPUs and forming strategic alliances with chip manufacturers, a16z creates a gravity well that attracts the most ambitious founders who cannot afford to wait in line for server capacity.

Their 2025 activity is distinguished by a sophisticated bifurcation of their capital. On one end, they are deploying billions into foundation models and infrastructure. On the other, they have developed a nuanced "Prosumer" thesis for the application layer. By analyzing spend data from fintech platforms like Mercury, a16z identified a critical trend: the early adopters of AI tools are not Fortune 500 CIOs but "prosumers" and early-stage startups. These smaller, agile entities are purchasing AI-native tools for coding, design, and marketing at unprecedented rates, creating a bottom-up adoption curve that mirrors the early days of SaaS.

Why They Are a Top Pick: a16z is the only firm effectively playing "Full Stack" venture capital in 2025. They are funding the nuclear power plant (energy), the GPU cluster (compute), the foundation model (intelligence), and the end-user application (consumption).

2. Sequoia Capital

2025 Investment Thesis: "The Cognitive Enterprise and The Reasoning Layer." Sequoia is focused on the transition from "Generative AI" (creating text/images) to "Reasoning AI" (planning/executing tasks), betting heavily on the "Agentic Workforce."

Strategic Analysis: Sequoia’s dominance in 2025 is rooted in its ruthlessly efficient management of the "AI Supply Chain." Having been early investors in Nvidia and OpenAI, they sit at the apex of the value chain. In late 2025, their strategy has shifted toward "Concentrated Conviction." Rather than spraying capital across hundreds of seed bets, Sequoia is doubling down on the "winners" of the 2023/2024 vintage, participating in secondary markets to consolidate ownership in generational companies.

The firm is particularly focused on the "Reasoning Layer." They argue that the next trillion dollars of value will not come from chatbots that can write poetry, but from systems that can "think" over long time horizons. This thesis drives their investments in companies like Harvey (legal AI) and other vertical-specific agents that require high-fidelity reasoning capabilities. They are effectively funding the "brains" of the enterprise.

Why They Are a Top Pick: Sequoia is the bridge between the "Old Guard" of Silicon Valley and the "New Guard" of AI. Their ability to secure allocation in the most competitive rounds while simultaneously identifying vertical applications like Harvey makes them indispensable.

3. Thrive Capital

2025 Investment Thesis: "Capital as a Moat for Deep Tech." Thrive believes that in the Foundation Model era, the primary differentiator is the ability to sustain massive capital burns to achieve "escape velocity" in model performance and distribution.

Strategic Analysis: Thrive Capital has redefined the role of a venture firm in 2025, acting less like a traditional VC and more like a private quasi-sovereign wealth fund. They have been the primary architect of the "Privatized IPO," leading massive multi-billion dollar rounds for OpenAI and Isomorphic Labs. By writing checks that range from hundreds of millions to billions, Thrive allows deep-tech companies to stay private indefinitely, avoiding the short-term pressures of the public markets while operating with the balance sheets of Fortune 50 companies.

Their 2025 portfolio construction is highly concentrated and strategic. Beyond OpenAI, they have taken significant positions in "Scientific Superintelligence," such as Isomorphic Labs (AI for drug discovery), co-leading rounds with deep-tech giants. This signals a belief that the next wave of AI value will be in "Atoms, not Bits"—applying intelligence to biology, chemistry, and physics.

Why They Are a Top Pick: Thrive has proven that "valuation sensitivity" is a losing strategy in a power-law market. By paying the highest prices for the absolute best assets, they have secured a position that no value-investing VC can challenge.

4. Index Ventures

2025 Investment Thesis: "The Transatlantic Bridge and Data Sovereignty." Index is betting on the arbitrage between European technical talent (mathematically rigorous, capital-efficient) and US commercial scaling power, while capitalizing on the fractured regulatory landscape.

Strategic Analysis: Index Ventures has carved out a unique niche by dominating the "Data Lifecycle" of AI. Their early and continued conviction in Scale AI demonstrates a prescient understanding that data labeling and reinforcement learning from human feedback (RLHF) are the oil refineries of the AI age. In 2025, they are leveraging this "Data Advantage" to fund the next generation of Enterprise AI applications.

Their strategy is distinctly transatlantic. With hubs in London, Paris, and San Francisco, Index is the go-to firm for European founders looking to flip to the US market. They are aggressive investors in "Sovereign AI" models—AI companies that build models compliant with specific regional regulations (like the EU AI Act), turning what many see as a regulatory burden into a competitive moat.

Why They Are a Top Pick: Index is one of the few firms explicitly targeting the "Safety and Governance" layer as a profit center. They understand that as AI becomes regulated, the tools that validate, red-team, and insure these models will become mandatory infrastructure.

5. Benchmark

2025 Investment Thesis: "The Contrarian Application Layer." Benchmark rejects the "capital cannon" approach of Thrive/a16z, focusing instead on finding "capital-efficient" AI anomalies that can achieve dominance without raising billions in compute costs.

Strategic Analysis: Benchmark remains the purist’s venture firm. In a year defined by $10 billion rounds and massive dilution, Benchmark is hunting for the outliers—the companies building highly specific, defensible workflows that do not require training foundational models from scratch. They are betting against the commoditization of intelligence, arguing that proprietary workflow data—not the model weights—is the only enduring moat.

Their recent activity involves backing companies that use "Small Language Models" (SLMs) or highly optimized fine-tuned models to solve specific business problems, such as automated coding or high-fidelity video generation (e.g., Fireworks AI). By focusing on the application layer that sits above the commoditized model layer, they aim for traditional venture returns (100x) rather than just index-fund-like exposure to the category winners.

Why They Are a Top Pick: Benchmark is the "anti-hype" investor. If a16z is funding the industrial revolution, Benchmark is funding the artisans who know how to use the new machines to create masterpieces.

6. Menlo Ventures

2025 Investment Thesis: "The Modern AI Stack." Menlo has codified the architecture of 2025, investing in the specific components (Vector Databases, Orchestration, Observability) that allow enterprises to actually put LLMs into production.

Strategic Analysis: Menlo Ventures has established intellectual leadership with their Modern AI Stack framework, a four-layer blueprint for enterprise adoption.

Layer 1 (Compute/Foundation): Investments in Anthropic.

Layer 2 (Data): Investments in Pinecone (Vector DB) and Unstructured (ETL).

Layer 3 (Deployment): Orchestration tools.

Layer 4 (Observability): Tools to monitor model drift and hallucinations.

Their 2025 "State of Generative AI" report indicates a decisive shift in their capital deployment toward "Reasoning Engines" and "Agentic Orchestration." They argue that the UI layer of AI is disappearing, replaced by invisible middleware that connects disparate business systems. Consequently, they are heavy investors in the "Deployment Layer"—tools that manage prompts, context windows, and model routing.

Why They Are a Top Pick: Menlo is the "Chief Architect" of the VC world. They are not just betting on horses; they are designing the racetrack. Their deep technical diligence ensures they are funding the components that are strictly necessary for the stack to function.

7. Lightspeed Venture Partners

2025 Investment Thesis: "Global Multi-Modal Scale." Lightspeed is focused on the convergence of modalities—video, audio, code, and text—and the platforms that can serve these across global markets, particularly Asia and the US.

Strategic Analysis: Lightspeed has been a quiet but massive force in the 2025 landscape, participating in the mega-rounds for Anthropic alongside major tech companies. Their distinction lies in their global footprint. While other VCs focus heavily on Silicon Valley, Lightspeed is actively arbitraging innovation between India, China, Israel, and the US, funding "Applied AI" companies that can serve non-English speaking markets.

Their portfolio includes significant bets on "Generative Media"—platforms that are replacing traditional content creation studios with AI pipelines. They view the "cost of creation" dropping to zero as a massive opportunity for new media networks to emerge. Investments in companies like ElevenLabs (Generative Audio) demonstrate their belief in the "Synthetic Senses"—AI that can speak, hear, and see with human fidelity.

Why They Are a Top Pick: Lightspeed is the "Globalist" investor. They understand that AI is a global phenomenon and that the winners in "Application AI" may not necessarily come from San Francisco, but from Tel Aviv, Bangalore, or London.

Part II: The Application Specialists (The Workhorses)

This group represents the investors who believe the infrastructure war is largely settled (or too expensive to fight) and that the real returns will come from the "Application Layer." Their focus is B2B, Vertical SaaS, and the transformation of services into software. They are hunting for the "Killer App" that justifies the billions spent on GPUs.

8. Emergence Capital

2025 Investment Thesis: "Coaching Networks and Deep Collaboration." Emergence believes that AI should not replace humans but "coach" them. They invest in "Coaching Networks"—software that learns from the best workers in a company and democratizes that knowledge to the rest.

Strategic Analysis: Emergence Capital has cultivated one of the most refined theses in the industry: The Emergence Rate. This metric measures how quickly an AI application evolves based on user interaction. In 2025, they are rigorously avoiding "thin wrappers" in favor of "Deep Collaboration" tools where AI is embedded in the workflow of sales, legal, and logistics.

Their investment philosophy centers on "Proprietary Business Data." They believe that the only way to defend against Open Source models is to have access to data that exists nowhere else—specifically, the "exhaust" data of human work (emails, edits, negotiations). Their portfolio companies, such as Ironclad and other vertical-specific platforms, utilize this data to create "High-Trust" AI. In regulated industries, hallucinations are liability; Emergence funds systems that keep humans in the loop for final verification, ensuring compliance while boosting productivity.

Why They Are a Top Pick: Emergence is betting on the "Blue Collar AI" revolution—bringing AI coaching tools to field service workers, construction managers, and logistics coordinators, areas largely ignored by the text-focused LLM giants.

9. Redpoint Ventures

2025 Investment Thesis: "From SaaS to Service-as-Software." Redpoint argues that the SaaS business model (selling seats) is dying, replaced by "Service-as-Software" (selling outcomes). They invest in AI agents that perform the job, not just the tool.

Strategic Analysis: Redpoint’s "InfraRed" is a staple of the industry, and their 2025 update highlights a massive pivot toward "Agentic Infrastructure." They are funding the enabling layers that allow agents to browse the web, use credit cards, and execute legal contracts autonomously.

Their shift to "Service-as-Software" is profound. Instead of funding a CRM software that a salesperson uses, they fund an "AI Sales Development Rep" that charges per meeting booked. This changes the revenue quality and unit economics of their portfolio, aligning them closer to services margins initially but scaling like software eventually. They view "Reverse ETL" (moving data from warehouses back into apps) as critical for these agents. Agents need state and context; Redpoint is funding the plumbing that feeds real-time business state to autonomous agents.

Why They Are a Top Pick: Redpoint is the "Business Model Innovator." They are helping founders redesign how they charge for software in an age where time-based billing is obsolete.

10. Greylock

2025 Investment Thesis: "Intelligent Applications & The Cybersecurity Agent." Greylock is betting that the most immediate, high-value application of AI agents is in cybersecurity and defensive posture management.

Strategic Analysis: Under partners like Saam Motamedi, Greylock has aggressively targeted the intersection of AI and security. In 2025, as AI-generated cyberattacks (phishing, deepfakes) increase, Greylock is funding the AI Defense layer - autonomous agents that patrol networks, patch vulnerabilities, and negotiate with threats in real-time.

Beyond security, Greylock is pioneering the "outcome-based" pricing model in their investments. They are backing companies like Adept and Cresta that are not priced per user but per "successful interaction," forcing startups to prove utility immediately. Their thesis on "The End of the Interface" suggests that future B2B software won't have a GUI but will simply be a command line or voice interface where users state a goal, and the software executes it in the background.

Why They Are a Top Pick: Greylock is bridging the gap between the "Enterprise Old Guard" (having backed Palo Alto Networks) and the "AI New Guard." They know how to sell AI to the CISO (Chief Information Security Officer).

11. Insight Partners

2025 Investment Thesis: "Process is the Moat." Insight Partners focuses on "ScaleUps"—companies that have found product-market fit and need to operationalize. They believe AI’s true value is in rewiring the "messy middle" of enterprise operations.

Strategic Analysis: Insight is the volume player of the growth stage. Their ScaleUp:AI and internal data teams give them a bird’s-eye view of what is actually being deployed in the Fortune 500, versus what is just being tested. In 2025, they are funding "System of Intelligence" companies—platforms that sit on top of Systems of Record (like Salesforce or SAP) and provide the reasoning layer.

They are actively advising their portfolio to pivot from "Copilots" (which require human initiation) to "Autopilots" (which run autonomously). Their capital is directed toward companies that can prove they reduce OpEx (Operating Expense) for their customers by at least 30%. They are heavily investing in "Code Modernization" agents—AI that maintains, refactors, and updates legacy enterprise codebases (COBOL, Java) automatically, solving a trillion-dollar technical debt problem.

Why They Are a Top Pick: Insight is the "pragmatist" of the group. They don't care about AGI (Artificial General Intelligence); they care about ARR (Annual Recurring Revenue) and operational efficiency.

12. Radical Ventures

2025 Investment Thesis: "Physical AI and Scientific Discovery." Radical Ventures differentiates itself by focusing on AI that interacts with the physical world (Robotics) and AI that accelerates science (Material Science, Biology).

Strategic Analysis: Based in Toronto but globally active, Radical is deep in the "Godfather of AI" ecosystem (tied to Geoffrey Hinton’s lineage). In 2025, they are one of the few firms boldly funding "Robotic Foundation Models"—AI brains that can control general-purpose humanoid robots.

They are also heavy investors in "AI for Science," funding companies using diffusion models to invent new proteins and materials. They believe this sector is immune to the "churn" of consumer apps. A prime example of their unique thesis is their backing of FireSat, a satellite constellation using AI to detect wildfires, which was named one of TIME's Best Inventions of 2025.

Why They Are a Top Pick: Radical is betting on "Sensory AI"—the ability of models to understand not just text, but infrared, radar, and hyperspectral data. They are funding the AI that will save the planet, not just write emails.

13. Point72 Ventures

2025 Investment Thesis: "Defense Tech and The Industrial Backbone." Backed by Steve Cohen, Point72 brings a hedge fund’s discipline to VC, focusing on AI for national security, defense, and heavy industry.

Strategic Analysis: Point72 Ventures is filling the gap left by traditional VCs who are wary of "dual-use" technologies (technologies with both civilian and military applications). In 2025, with geopolitical instability high, they are funding AI for Command and Control, autonomous drone swarms, and intelligence analysis platforms.

They also focus heavily on "Vertical FinTech," using AI to automate the complex, paper-heavy back offices of insurance and banking. Their "buy vs. build" analysis for AI infrastructure is rigorous, often advising companies to use open-source models on private infrastructure rather than relying on OpenAI to maintain data secrecy.

Why They Are a Top Pick: Point72 represents "Smart Money" in the truest sense. They leverage the massive data capabilities of their hedge fund parent to validate the claims of the startups they invest in.

14. Founders Fund

2025 Investment Thesis: "The American Dynamism & Hard Tech Renaissance." Founders Fund continues to champion the "contrarian" view that AI must be applied to "Hard Tech"—manufacturing, defense, and energy—rather than just software bits.

Strategic Analysis: Having led one of the largest fundraising efforts in H1 2025 ($4.6 billion vehicle), Founders Fund is armed with a war chest to back high-capex, high-risk ventures. Their thesis aligns closely with "American Dynamism," investing in companies that support the US national interest. In 2025, this means funding AI-driven defense contractors (competing with Anduril), nuclear fusion startups using AI for plasma control, and next-gen space companies.

They are skeptical of the "consensus" AI trade (SaaS wrappers) and are looking for "Zero to One" innovations. They are aggressive in backing "Sovereign Intelligence"—tech that ensures Western supremacy in the AI arms race.

Why They Are a Top Pick: Founders Fund is the "Patriot" investor. They are funding the technologies that will define the geopolitical balance of power in the 21st century.

Part III: The Seed & Scrappy (The First Believers)

These firms are the high-volume risk-takers. They are not writing $100M checks; they are writing the first $500k to $2M check that allows two engineers with a laptop to challenge Google. They are the feeders of the ecosystem.

15. Y Combinator

2025 Investment Thesis: "The Factory of AI-Native Startups." YC remains the premier accelerator, betting on volume and the "young genius" archetype. Their 2025 batches are dominated by AI agents, robotics, and dev tools.

Strategic Analysis: YC is the volume leader of the industry. In Q3 2025 alone, they participated in over 200 seed deals, making them the most active seed investor globally. Their thesis has shifted toward "Blue Ocean" AI—encouraging founders to build AI for unglamorous verticals like procurement, government contracting, and shipyards.

They are systematically funding "AI for Legacy Industries." Recent batches have featured startups building AI for ship manifests, AI for concrete pouring, and AI for dental billing. They are also the primary incubator for "Open Source" commercialization, funding the maintainers of popular libraries to turn them into companies.

Why They Are a Top Pick: YC is the best barometer for what is happening at the "garage" level of innovation. If you want to know what will be hot in 2027, look at the YC batch of 2025.

16. Conviction (Sarah Guo)

2025 Investment Thesis: "Software 3.0." Sarah Guo’s firm is built on the premise that "Software 3.0" is code written by data, not humans. She invests in "AI-Native" founders who are reimagining workflows from scratch.

Strategic Analysis: Conviction is a specialist firm. Sarah Guo (formerly Greylock) has deep technical fluency and funds companies that are often "too research-heavy" for generalist seed funds but "too early" for Series A. Her investments in companies like Cognition (creators of Devin) and Mistral show an uncanny ability to spot technical outliers before the consensus forms.

She is actively looking for "Cognitive Architectures"—new ways to structure LLMs to reason over long time horizons. Her podcast, "No Priors," serves as a deal-flow engine, attracting the most technical founders who want an investor who can actually read their whitepapers.

Why They Are a Top Pick: Conviction is the "Founder’s VC." Sarah Guo understands the "metal" of the models and supports founders who are building technical moats, not just sales moats.

17. Elad Gil

2025 Investment Thesis: "The Solo Capitalist Titan." Elad Gil operates as a one-man institution, betting heavily on high-growth breakouts with a network-driven approach.

Strategic Analysis: Elad Gil is often the first call for "repeat founders." His portfolio (Perplexity, Harvey, Pika) reads like a "Who’s Who" of the 2025 AI unicorn list. He is currently advising founders to avoid "The Messy Middle"—advising them to either build massive foundation models or highly specific vertical apps. He warns that everything in between will get crushed by Big Tech.

His 2025 investments have focused on "AI Infrastructure" and "Health Tech," participating in rounds for companies like Helsing (defense AI) and various stealth bio-AI startups. He operates with speed, often making decisions in days, which appeals to hyper-growth founders.

Why They Are a Top Pick: Elad Gil provides the signal. When he invests, the rest of the market pays attention. He is the ultimate "Super Angel" with the firepower of a VC fund.

18. Air Street Capital

2025 Investment Thesis: "The State of AI Reality." Air Street is known for its annual "State of AI" report. They invest in "AI-first" companies with a heavy focus on Europe and technical differentiation.

Strategic Analysis: Air Street avoids the hype. Their diligence process is notoriously technical. In 2025, they are funding "Bio-bits"—the intersection of biology and AI bits—and are skeptical of generic generative media. They are looking for "industries that still use fax machines" and applying state-of-the-art computer vision and NLP to revolutionize them.

Their 2025 report highlights a shift toward "Pragmatic Safety". They believe that safety research is entering a pragmatic phase where models can imitate alignment under supervision, and they are funding the tools that make this possible.

Why They Are a Top Pick: Air Street is the "Academic" investor. They bridge the gap between the research lab and the boardroom, ensuring that the science is sound before the check is written.

19. Zetta Venture Partners

2025 Investment Thesis: "AI Native from Day Zero." Zetta only invests in AI. They look for companies where the AI is the product, not a feature.

Strategic Analysis: Zetta is the first specialized AI fund. They have moved aggressively into "AI for Industrials" and "AI for Climate." They believe the next wave of AI is not in generating text, but in simulating physical systems (e.g., weather, fluid dynamics for engineering) to accelerate R&D in the physical world. Their "AI Native" conference series positions them as thought leaders in the space, gathering the community of "non-wrapper" founders.

Why They Are a Top Pick: Zetta is the "Specialist." They don't do crypto, they don't do consumer social. They only do AI, giving them a depth of expertise that generalist funds cannot match.

20. Amplify Partners

2025 Investment Thesis: "The Machine Learning Engineer's Toolkit." Amplify invests in the tools that build the AI. They believe the "AI Engineer" is the new "Software Engineer."

Strategic Analysis: Amplify is the go-to for MLOps and developer tools. They are funding the "picks and shovels" for the new stack—tools for evaluating model hallucinations, managing prompt libraries, and synthetic data generation. Their "State of AI Engineering" survey gives them proprietary insight into what tools engineers actually love and use in production. They champion the "practitioner turned founder," backing engineers who are solving their own problems.

Why They Are a Top Pick: Amplify is the "Engineer's Choice." They understand the plumbing of AI better than anyone else and invest in the tools that keep the lights on in the AI factory.

Part IV: The "Red Flags" — What VCs Are NOT Funding in 2025 (The Anti-Portfolio)

To provide maximum value to founders and investors, it is crucial to understand the "Anti-Portfolio"—the sectors and business models that sophisticated investors are actively avoiding in late 2025. These areas are considered "toxic assets" due to regulatory risk, lack of defensibility, or market saturation.

1. The "Thin Wrapper" and Generic UIs

The era of raising a Series A for a "ChatGPT for X" is definitively over. VCs now view "Thin Wrappers"—applications that rely entirely on a third-party model (like GPT-5) with no proprietary data or workflow stickiness—as uninvestable.

The Risk: The "Feature vs. Product" dilemma. The underlying model providers (OpenAI, Google, Microsoft) are aggressively moving up the stack, releasing features that kill wrapper startups overnight. For instance, OpenAI’s release of native PDF analysis killed dozens of "Chat with PDF" startups instantly.

VC Sentiment: "If OpenAI can build your product in a weekend, we can't invest."

2. Generative Media with Copyright Liability

Investors are extremely skittish about generative music, video, or image platforms that cannot prove they have licensed their training data. The legal battles of 2025 (such as Bartz v. Anthropic) have created a "Regulatory Overhang" that scares off capital.

The Case Law: High-profile cases have demonstrated that courts are scrutinizing "Fair Use" claims. While some rulings have been mixed, the risk of a "Model Disgorgement" order—where a court forces a company to delete its algorithm because it was trained on fruit of the poisonous tree—is a fatal risk for VCs.

The Pivot: Investors now prefer "Ethical AI" media tools that have clear licensing deals with rights holders (e.g., models trained on Adobe Stock or Getty Images) or tools that assist human creators rather than replacing them.

3. The "Copilot" for Saturated Verticals

While "Agents" are hot, "Copilots" (assistants that sit in a sidebar) are seeing diminishing returns in saturated markets like general coding or general writing assistance.

The Saturation: Tools like GitHub Copilot and Cursor have locked up the developer market. New entrants trying to build a "better autocomplete" face insurmountable distribution hurdles.

The Risk: VCs want "Systems of Work" that own the entire process, not just a helper tool. If your product is just a sidebar in Microsoft Word, Microsoft will eventually build it for free. The demand is for "Autonomy," not "Assistance".

Conclusion: The Deployment Era and the Road to 2026

The funding environment of late 2025 is vibrant but unforgiving. The "spray and pray" tactics of the early 2020s have been replaced by a sniper-like focus on infrastructure durability and application utility. The 20 firms listed above control the narrative and the purse strings of this new era.

The data indicates that we are entering a "Deployment Era." The infrastructure is being laid, the models are reaching reasoning maturity, and the capital is now flowing to the companies that can use these tools to rewire the global economy. The "Great Decoupling" will likely widen in 2026—the gap between the "AI Haves" (those with proprietary data and compute) and the "AI Have-Nots" (generic wrappers) will become insurmountable.

For founders, the mandate is clear: Build for "Agency," secure proprietary data, and ensure your product does real work. For investors, the opportunity lies not in chasing the hype, but in identifying the infrastructure that powers this shift and the vertical applications that can effectively capture value from it.

To filter through the noise view the complete feed of funding rounds at Roundly.io

Check out my other blog posts:

Nov 17

Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

Nov 15

Top AI Investors 2025 YTD by Dollars and Deal Count

Nov 14

AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market