The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

Executive Summary

The global Artificial Intelligence ecosystem in 2025 presents a landscape of profound contradictions and immense strategic importance. While the market is populated by a vast number of participants—approximately 33,089 AI companies globally—a closer analysis reveals a market structure defined by intense capital concentration, escalating geopolitical tensions, and critical infrastructural bottlenecks.

Global AI funding has surged by an extraordinary 1,632% since 2013, reaching a total of $252.33 billion in 2024. However, this capital is not evenly distributed.

A 'commercialization paradox' has emerged where, despite high company formation, venture capital deal volume has declined, with investment consolidating into massive 'megarounds' for a select few. This dynamic is set against a complex geopolitical backdrop. The United States, home to roughly 25% of all AI companies and attracting $109.1 billion in private AI investment in 2024, leads in commercial agility and market adoption. This is contrasted by China's strategic focus on foundational intellectual property; as of 2023, China held 69.7% of all granted AI patents, with Baidu alone possessing nearly 19,000 patent families. This creates a fundamental tension between near-term commercial dominance and long-term control via IP and standards.

Underpinning this entire ecosystem is a looming infrastructural constraint. The computational demands of training and deploying advanced AI models are driving an unprecedented need for energy. Projections indicating that U.S. data center power demand could grow by 160% by 2030 reveal that access to power and compute are becoming the ultimate barriers to entry, creating a structural advantage for hyperscalers and the most heavily funded startups.

Section 1: The Commercialization Paradox: Proliferation Meets Consolidation

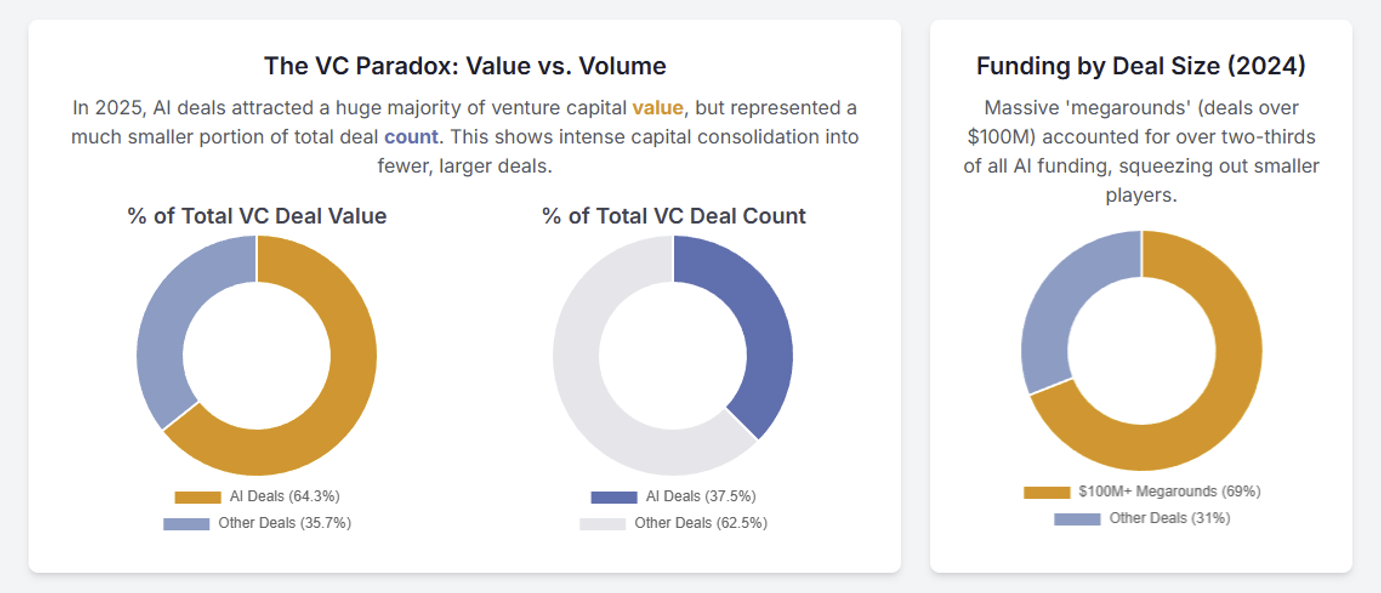

The AI market exhibits a significant 'commercialization paradox' where a large and growing number of companies (approximately 33,089 globally) coexists with a broader venture capital market trend of declining deal volume, which has hit lows not seen since Q4 2017. This apparent contradiction is explained by an intense concentration of capital. While the total number of investment 'bets' may be shrinking, the value of those bets in AI is exploding. Capital is not being spread thinly; instead, it is being consolidated into massive 'megarounds' for a select group of mature, market-leading AI companies. This reflects the market's maturity and the immense capital required for computationally expensive tasks like training foundational models, creating a bifurcated landscape of many small players and a few hyper-funded giants.

Mega-round Economics: 69% of AI Dollars in $100M+ Deals

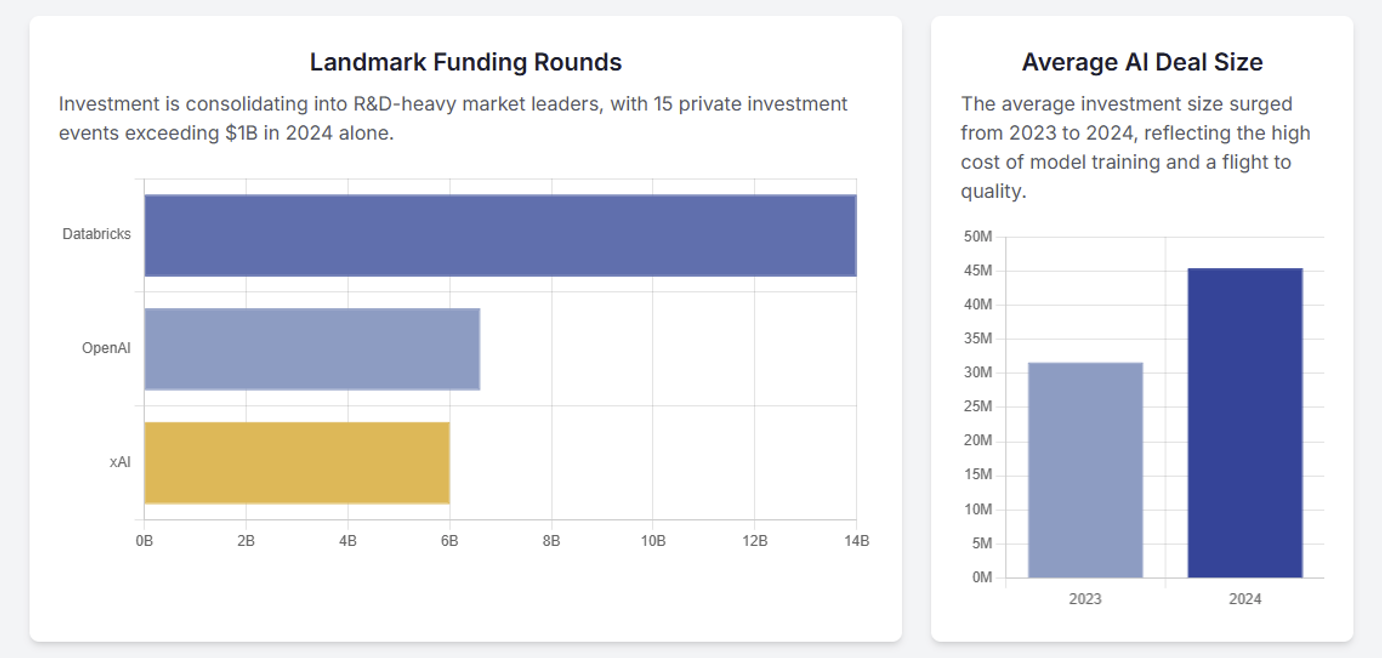

Capital in the AI sector is heavily consolidating. The average size of a global AI private investment event surged from $31.6 million in 2023 to $45.4 million in 2024. In 2025, AI startups attracted $89.4 billion in global venture capital, representing 34% of all VC investment despite comprising only 18% of funded companies.

This concentration is driven by 'megarounds' (deals of $100M or more), which accounted for 69% of all AI funding in 2024. The number of such deals reached 89 in 2024, a 38% increase from 2023. This trend continued into 2025, with VCs averaging over 100 megadeals per quarter, a level not seen since 2021 and 2022.

Survivorship Bias: 15 $1B+ Raises vs. Widespread Seed-Stage Rationing

The flight to quality is stark. In 2024, there were 15 private AI investment events that exceeded $1 billion. Landmark R&D-heavy funding rounds further illustrate this, with Databricks securing approximately $14 billion, OpenAI raising $6.6 billion, and xAI raising $6 billion. In Q3 2025 alone, nine billion-dollar-plus financings accounted for nearly 40% of the quarter's total deal value, emphasizing the stark difference between the "haves and have-nots." While a record-breaking $73.6 billion was raised by AI & ML startups in Q1 2025, this capital is flowing to a shrinking pool of perceived winners, leaving the long tail of the 33,089 AI companies to compete for a dwindling share of early-stage funding.

Section 2: The Geopolitical Axis: Commercial Agility vs. Foundational IP

The global AI balance of power is defined by a strategic tension between two competing models. The United States leverages its commercial agility, deep capital markets, and flexible regulatory environment to dominate in company formation and private investment. In contrast, China is executing a deliberate, long-term strategy focused on achieving dominance in foundational intellectual property (IP). This creates a geopolitical axis where the U.S.'s current market leadership is pitted against China's strategic positioning to control future standards and licensing.

U.S. Funding Engine and Commercial Dominance

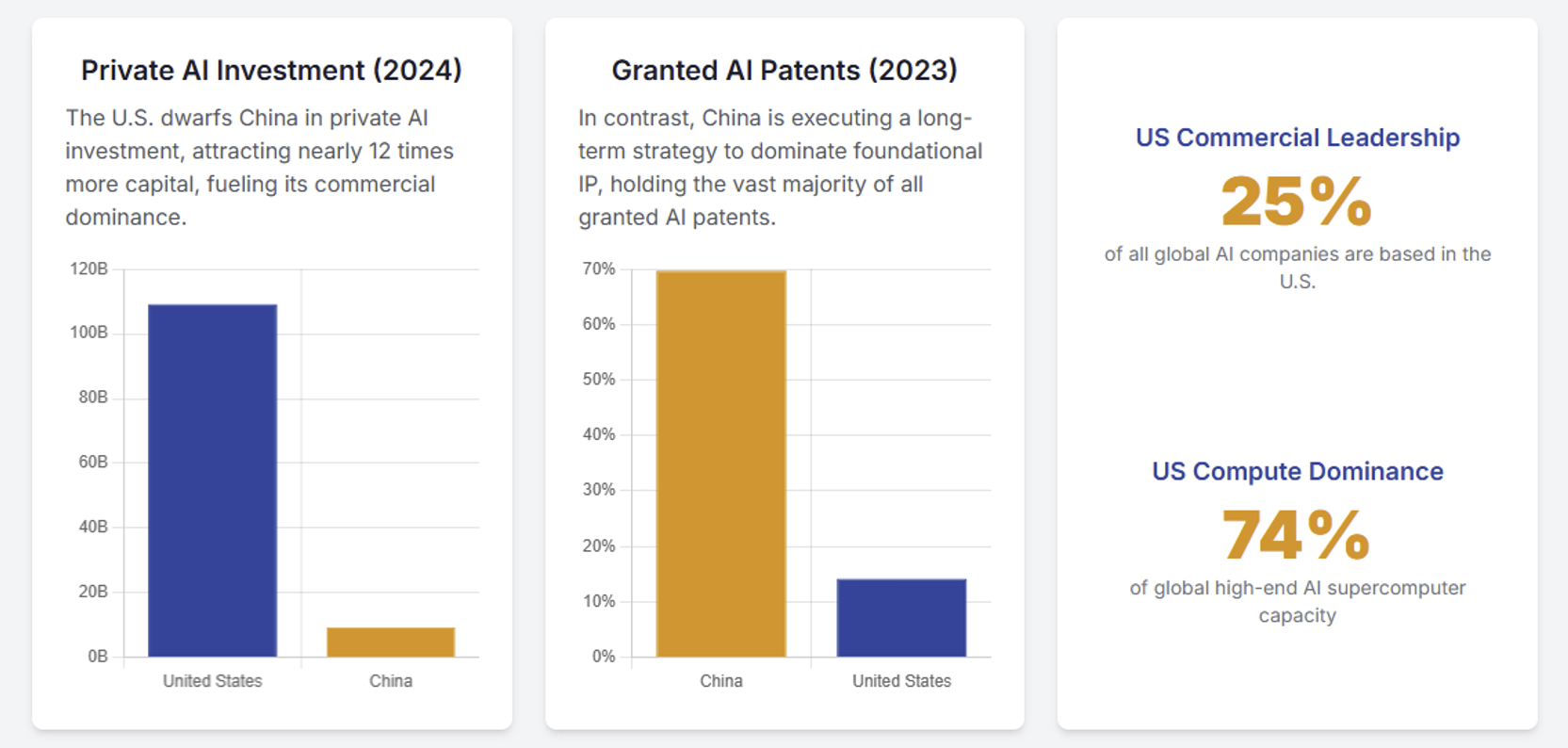

The United States leads in commercial AI adoption, hosting approximately 25% of the world's AI companies. This leadership is fueled by a market-driven, 'light-touch' regulatory environment that reduces barriers to entry and accelerates time-to-market. The U.S.'s dominance is cemented by its unparalleled access to capital; in 2024, it attracted a staggering $109.1 billion in private AI investment, nearly 12 times more than China's $9.3 billion. This funding has fostered a vibrant ecosystem, with the U.S. accounting for 1,073 newly funded AI companies in 2024, compared to just 98 in China. Furthermore, the U.S. dominates the physical infrastructure for innovation, controlling an estimated 74% of global high-end AI supercomputer capacity.

China's IP Arsenal and Standards Strategy

China's strategic approach is centered on dominating foundational IP as a long-term control mechanism. As of 2023, China held 69.7% of all granted AI patents worldwide, dwarfing the U.S. share of 14.2%. In the critical generative AI space, Chinese inventors filed over 38,000 inventions between 2014-2023, six times more than the U.S. The top three assignees for GenAI patents are all Chinese firms: Tencent, Ping An, and Baidu.

The Chinese technology giant Baidu is a prime example of this strategy. As of late 2023, Baidu had filed for over 19,000 AI patents, maintaining its leading position in China for six consecutive years. This volume-based strategy is a deliberate effort to shape future global AI standards and gain leverage in licensing negotiations for Standard-Essential Patents (SEPs), creating a strategic counterweight to U.S. commercial leadership.

Section 3: The Infrastructural Constraint: Compute, Energy, and Sustainability

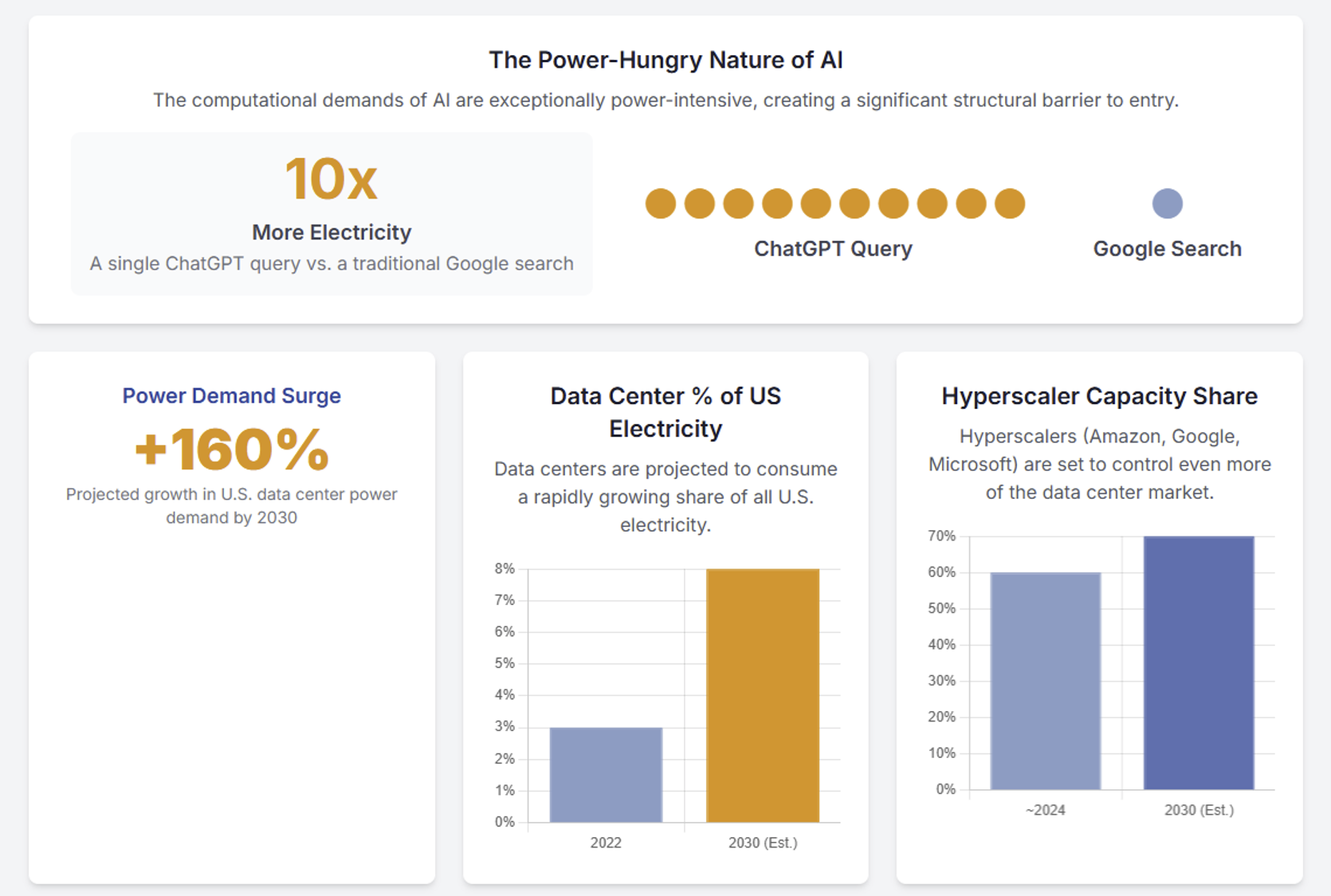

The massive and escalating costs for compute power and energy are creating formidable structural barriers to entry in the global AI market. The core of this constraint lies in the exceptionally power-intensive nature of AI workloads. A single ChatGPT query consumes nearly ten times the electricity of a traditional Google search. This voracious demand translates into enormous capital and operational expenditures that are far beyond the reach of most of the ~33,089 AI companies, effectively creating a moat that protects large incumbents.

The 160% Power-Demand Surge

The scale of this challenge is immense. Goldman Sachs Research estimates that U.S. data center power demand will grow 160% by 2030. By that year, data centers are projected to consume 8% of total U.S. electricity, up from 3% in 2022. The International Energy Agency projects that electricity demand from AI-optimized data centers alone could more than quadruple by 2030. This surge requires massive investment, with U.S. utilities needing to invest around $50 billion in new generation capacity just to support data centers.

Hyperscaler Advantage and Capacity Consolidation

These infrastructural constraints provide a profound and durable advantage to hyperscalers like Amazon, Google, and Microsoft. These entities possess the immense capital required to navigate the challenging energy landscape. Their share of data center capacity is projected to grow from 60% to 70% by 2030. They can strategically bypass public grid constraints by investing billions in private power solutions, including long-term Power Purchase Agreements (PPAs), on-site generation, and even advanced nuclear technologies like Small Modular Reactors (SMRs). This ability to secure multi-gigawatt power commitments creates a nearly insurmountable barrier for smaller competitors, solidifying the hyperscalers' role as the gatekeepers of the AI revolution. AI-dedicated data centers, designed for high power density and liquid cooling, are almost exclusively owned by these hyperscalers or wholesale operators.

Section 4: The Strategic Outlook: Where the Next Wave of Value Lies

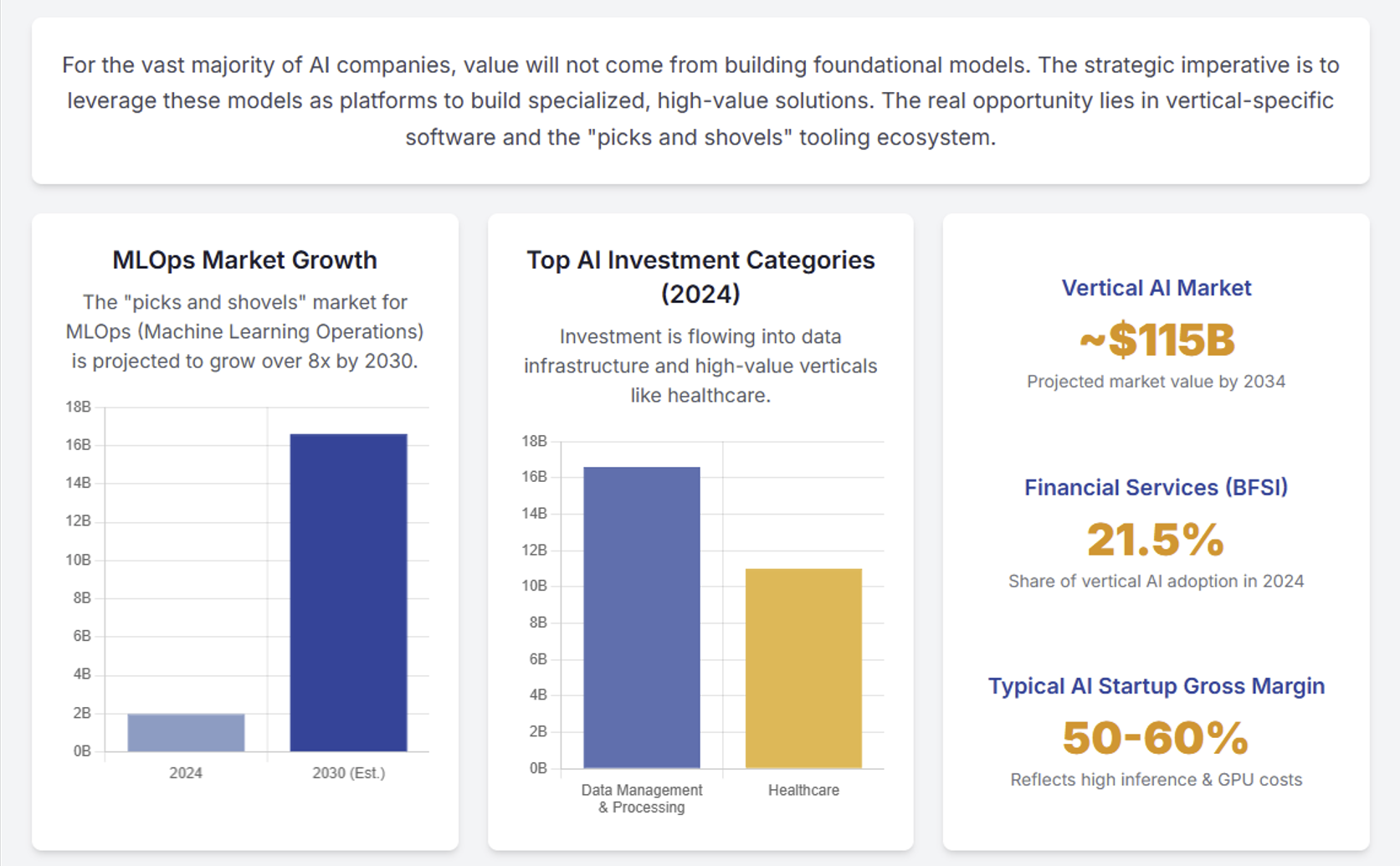

For the vast majority of the ~33,089 AI companies, future value creation will not be found in the capital-intensive race to build foundational models. The immense structural barriers—including prohibitive compute costs, severe energy constraints, and capital consolidation—make direct competition at the model layer untenable for most. The strategic imperative is to leverage the increasingly powerful foundational models as a platform upon which to build specialized, high-value solutions. Value will be captured by companies that focus on vertical-specific software, the MLOps and tooling ecosystem, and specialized services that solve tangible business problems.

The Vertical Software Opportunity

The most significant opportunity lies in creating vertical-specific AI solutions trained on proprietary datasets and deeply embedded into industry workflows. The market for vertical AI is projected to reach between $69.6 billion and $115.4 billion by 2034, expanding at a CAGR of over 21%.

Healthcare

This sector was a leading vertical for investment in 2024, attracting $11 billion. Companies like Abridge AI, which transcribes doctor-patient conversations and integrates with EMR platforms, demonstrate the power of combining deep domain knowledge with AI.

Financial Services (BFSI)

As the largest adopter of vertical AI in 2024 (21.5% share), this sector uses AI for fraud detection, algorithmic trading, and risk management. The complex regulatory environment creates high barriers to entry, making compliance-focused AI solutions highly defensible.

Legal & Compliance

Platforms like Harvey and Ironclad are automating contract analysis and due diligence, embedding themselves into the critical functions of law firms and corporate legal departments.

The MLOps and Tooling "Picks and Shovels" Opportunity

As AI scales from experimentation to production, a robust ecosystem of MLOps (Machine Learning Operations) and tooling has become critical. This layer provides the "picks and shovels" for the AI gold rush. The MLOps market was valued at over $2 billion in 2024 and is projected to grow to $16.6 billion by 2030 at a CAGR of over 40%.

Key opportunities include:

Data Infrastructure: 'Data Management and Processing' was the second-most invested AI category in 2024, attracting $16.6 billion. Companies like Scale AI provide critical infrastructure for data labeling and preparation.

Governance and Compliance: With the rise of regulations like the EU AI Act, platforms that help manage AI risk, ensure transparency, and automate compliance are in high demand.

Cost Optimization (FinOps): As inference costs become a major component of COGS, tools that help companies manage and optimize their cloud compute spend are becoming indispensable.

Guidance for Investors and Strategists

Given the market's structure, investors should prioritize the application layer over the foundational model layer:

Focus on Vertical AI: Seek companies with deep domain expertise and a clear strategy for building a proprietary data moat by embedding their solution into critical customer workflows.

Invest in the 'Picks and Shovels': The MLOps, tooling, and AI governance markets are poised for significant growth and have more predictable, SaaS-like business models.

Scrutinize Unit Economics: For AI startups, investors must perform deep diligence on gross margins (typically lower at 50-60%), the cost of inference, and the company's plan to manage GPU COGS.

Assess the Moat Beyond the Model: Defensibility rarely comes from the model itself. Focus on the strength of proprietary data feedback loops and workflow integration.

Hedge Against Infrastructure Constraints: Consider investments in the enablers of the AI boom, such as data center operators and power generation companies, to hedge against infrastructure bottlenecks.

Recommended:

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 17

Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

Nov 15

Top AI Investors 2025 YTD by Dollars and Deal Count

Nov 14

AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market