Top AI Investors 2025 YTD by Dollars and Deal Count

What changed in 2025 YTD is where the dollars concentrated and who controls access. Capital clustered around a small group of funds backing compute, chips, and the tools teams work in daily, while application rounds multiplied by count. That’s why one deal—OpenAI’s $40B round—reshapes the dollars leaderboard, but not the deals leaderboard. And it’s why reported totals like ~$192.7B YTD in AI funding matter less than who’s writing the gatekeeping checks.

TL;DR: The State of AI Investing in 2025

Record inflow, but concentrated: AI startups have raised roughly $192.7B YTD with mega‑rounds driving most of it.

Mega‑round gravity: One‑off outliers like OpenAI’s $40B can move quarterly venture totals on their own; treat dollar ranks as outlier‑sensitive.

Two different winners: Dollars board ≠ deals board. Use both to separate gatekeepers (late‑stage dollars) from access builders (volume across stages).

Infra soaks the dollars: Most capital went to models, chips, and data centers; facilities/JVs (for example, the Meta–Blue Owl $27B DC JV) are material to the ecosystem but excluded from equity totals.

Leaderboards: Who Tops 2025 So Far?

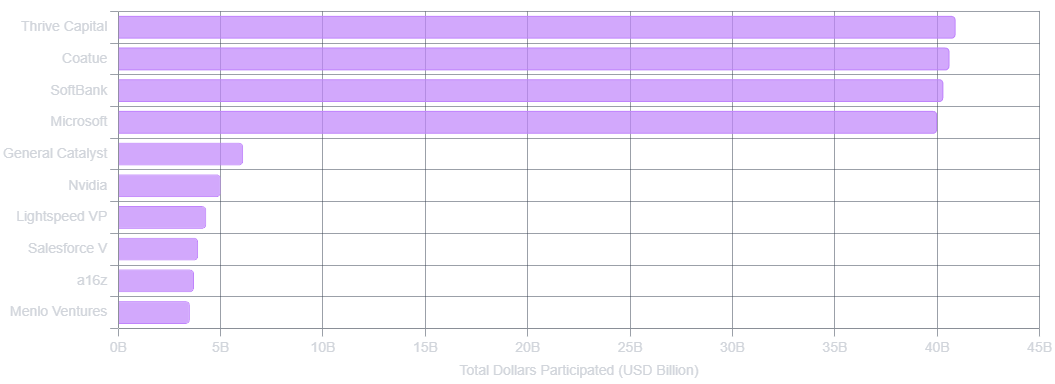

Method note (read this first): “Total dollars participated” credits the full round to each listed investor. It’s a standard proxy for involvement but double‑counts by design. Treat it as a power‑signal for late‑stage access, not as a net‑new capital measure.

Top 10 Investors by Total Dollars Participated (YTD 2025)

What this signals:

Late‑stage pricing power is concentrated. If your round depends on a short list of mega‑funds, your timing and proof points matter more than comps.

Sensitivity check: Remove OpenAI’s $40B and the top four by dollars reshuffle materially; treat this board as an “access map,” not a scoreboard of dry powder.

Facilities/JVs (for example, Meta–Blue Owl $27B) don’t belong here, but they explain why infra‑adjacent software still finds budgets even in tighter late‑stage markets.

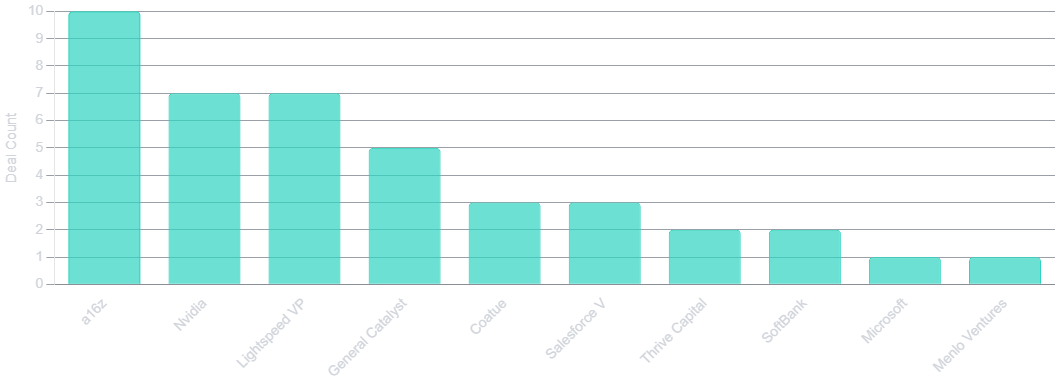

Top 10 Investors by Deal Count (YTD 2025)

What this signals:

Founders: Pitch the dollars board for big, late rounds; pitch the deals board for speed, intros, and multi‑stage support.

Undisclosed early rounds depress dollar ranks but still build signal and access—expect the deals board to lead on net‑new surfaces (agents, verticals) before dollars catch up.

Strategics like Nvidia and Salesforce Ventures bring distribution and infra access that can matter more than check size at certain stages.

Reading the Tables: How Mega‑Rounds Skew Perception

The dollars board is an outlier meter. A single participation in a $40B round can outweigh a year of steady activity, which is why dollars leaders and deal‑count leaders rarely match. Treat the two lists as complementary lenses: one shows who can set late‑stage terms, the other who sees the most experiments early and often.

Callout: Facilities ≠ VC. Asset‑level financing like the Meta–Blue Owl $27B data‑center JV belongs in the story of AI’s buildout, but keeping it out of equity totals keeps apples with apples. Still, those megawatts and interconnect dollars shape which software budgets open next quarter.

Deep‑dive analysis

Sensitivity to mega rounds: If you strip out the OpenAI $40B raise, the dollars leaderboard reshuffles quickly. That is the point. Treat the dollars view as a map of late‑stage access and pricing power. It will swing with a few outliers like OpenAI’s round (see TechCrunch) and stay steadier in the deal‑count view, where breadth matters more than single checks.

What the leaders are signaling

Late‑stage gatekeepers are setting terms on compute, chips, and core tooling. That is why record totals like Bloomberg’s ~$192.7B YTD matter less than who can actually clear a multi‑billion round.

Strategics with distribution and infrastructure matter even when the check is smaller. Nvidia and Salesforce Ventures bring access that can outweigh dollars at certain stages.

Facilities and joint ventures shift software budgets with a lag. The Meta–Blue Owl $27B data‑center JV is not venture equity, yet it helps unlock spending on inference, orchestration, and data tooling a quarter or two later.

Key themes to watch next

Inference is where margins move. Training headlines pull attention, but the next wave of adoption depends on shaving latency and cost per request at scale.

Platformization in developer tools. Tools that own the edit‑to‑deploy loop graduate from “plugin” to “platform,” which is why late‑stage dollars cluster around a few environments teams live in every day.

Geography follows power and talent. The United States remains the center of gravity for AI funding, and a handful of hubs capture most of the late‑stage activity. Cross‑border money still shows up in the largest checks.

Methodology: Timeframe is Jan 1, 2025 through the most recent complete week. Scope includes AI‑core models, chips, inference/tooling, data infra, agents, and vertical AI apps; generic software is excluded. Included: priced equity rounds and clearly tied convertibles. Excluded: debt, credit, grants, and facility/JV financing. “Dollars participated” credits the full round to each investor (double‑counts). Amounts normalized to USD; undisclosed sizes count toward deals, not dollars.

FAQ:

• Why exclude facilities/JVs? Asset‑level financing isn’t venture equity.

• Why use “dollars participated”? Fast proxy for late‑stage access; it double‑counts.

• How often is this updated? After the most recent complete week.

Check out my other blog posts:

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 17

Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

Nov 14

AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market