Top 5 AI Investment Themes for 2026 (Backed by $216 Billion)

The artificial intelligence gold rush isn't slowing down; it's accelerating at a breathtaking pace. In 2025, global AI funding is on track to shatter all previous records, reaching an unprecedented projected total of $216 billion. This colossal wave of capital, however, signals more than just investor frenzy. It marks a pivotal shift in the AI revolution, moving from the era of pure experimentation with foundational models to a new phase of pragmatic, large-scale deployment.

This money is the fuel for the next generation of AI, which will be defined not by abstract potential, but by tangible, workflow-integrated applications and autonomous systems that are set to explode into the mainstream in 2026.

The $216 Billion Springboard: Why 2025's Funding Surge Matters

To understand where we're going, we first need to grasp the sheer scale of the capital flowing into AI. While different data providers report slightly different numbers due to varying methodologies and cut-off dates, the trend is undeniable.

The headline figure of $216 billion is a full-year projection from CB Insights. Meanwhile, PitchBook reported a firm year-to-date total of $192.7 billion as of early October 2025, a figure widely cited by outlets like Bloomberg. Crunchbase reported a lower figure, but its data cut-off was earlier in the year, missing a surge of late-quarter deals.

This influx is defined by several powerful trends:

Mega-Rounds Dominate: Deals over $100 million have constituted over 75% of total funding in the last four quarters.

Deal Sizes Soar: The average AI deal size has skyrocketed by 86% from 2024, now standing at $49.3 million.

US-Centric Capital: The United States has solidified its position as the epicenter of AI investment, attracting an overwhelming 85% of total global funding (Bloomberg).

This isn't just more money; it's smarter, more concentrated capital targeting specific, high-growth themes poised to redefine industries in 2026.

Five Themes Set to Explode in 2026

So, where is this historic war chest being deployed? Our analysis reveals five interconnected themes that are moving from the lab to the real world, fueled by billions in fresh capital.

1. AI Agents: From Copilot Assistants to Autonomous Coworkers

Why It's Exploding: The enterprise AI market is undergoing a fundamental shift from passive, human-prompted copilots to proactive, autonomous AI agents capable of executing complex, multi-step tasks with minimal oversight. This transition is driven by technical unlocks in 2025, including advanced planning, tool-use frameworks (like LangGraph and AutoGen), and persistent memory that allows agents to learn. Top VCs like Andreessen Horowitz and Bessemer Venture Partners have identified agents as a primary thesis, with market forecasts projecting spending on agentic AI to hit $155 billion by 2030. Enterprise adoption is already well underway, with a PwC survey finding 79% of US business executives are adopting AI agents and a McKinsey report indicating 23% of organizations are actively scaling them.

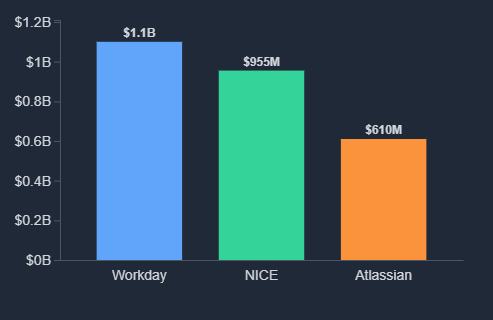

Backed by Billions: The strategic urgency was clear in 2025's M&A market. Three of the top five AI exits in Q3’25 were agent-related. This includes Workday's acquisition of Sana Labs for approximately $1.1 billion to create a "new front door for work," NICE's $955 million purchase of conversational AI leader Cognigy to deploy autonomous customer service agents, and Atlassian's $610 million acquisition of The Browser Company to build an agentic interface for SaaS.

2026 Prediction: 2026 will be the breakout year for enterprise agents. Gartner forecasts that a remarkable 40% of enterprise applications will be integrated with task-specific AI agents by the end of 2026, a dramatic leap from less than 5% in 2025. Expect the M&A frenzy to continue as software incumbents rush to buy, rather than build, these critical capabilities (CB Insights Q1’25).

2. Humanoid Robots: Hitting the Factory Floor at Human-Cost Parity

Why It's Exploding: The humanoid robot market is at a major inflection point, moving from R&D to initial commercial deployments. This is driven by acute labor shortages and the unique ability of humanoids to operate in "brownfield" environments (spaces designed for humans) without expensive retrofits. Critically, manufacturing costs plummeted by 40% year-over-year in 2025, making a humanoid unit competitive with a human worker's annual minimum wage. The rise of Robots-as-a-Service (RaaS) models, with pricing around $2,000 to $10,000 per month, is further lowering adoption barriers.

Backed by Billions: A "brutally expensive" global capital race validated this theme in 2025. Frontrunner Figure AI announced a $1.5 billion Series C at a staggering $39 billion valuation, backed by Microsoft, OpenAI, Nvidia, and Jeff Bezos. Other major players attracting huge investment include Agility Robotics (valued at $2.9 billion), UBTech Robotics (secured a $1 billion strategic financing facility), and Sanctuary AI.

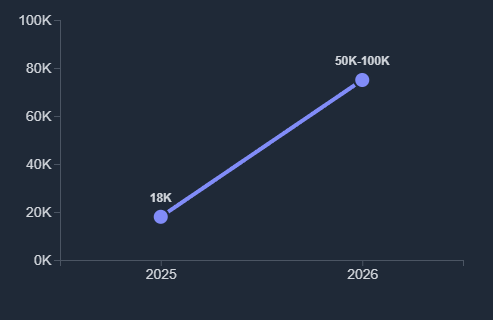

2026 Prediction: Global shipments of humanoid robots are forecasted to surge to between 50,000 and 100,000 units in 2026, up from an estimated 18,000+ in 2025. The 2026–2027 period will mark the beginning of scaled deployments beyond pilots, especially in logistics and automotive manufacturing. A key milestone will be the arrival of the first "cooperatively safe" certified humanoids, enabling closer collaboration with human workers.

3. The Open-Source AI Surge: From Community Project to Enterprise Powerhouse

Why It's Exploding: In 2025, open-source AI matured into a powerful commercial force. This was driven by clear standards (the OSI's Open Source AI Definition), regulatory tailwinds like the EU AI Act's exemption for open-source systems, and performance parity with closed-source models. Mainstream inference optimizations have made open models dramatically cheaper to run, fueling enterprise adoption by companies seeking customization, data residency, and cost-effectiveness. Deep integration into major cloud platforms like AWS Bedrock and Azure AI has made them a first-class option.

Backed by Billions: Massive, strategic investments in 2025 gave open-source leaders the capital to compete with proprietary giants. European champion Mistral AI raised a landmark €1.7 billion commitment from chip-equipment giant ASML. Additionally, Together AI, a specialized cloud for running open-source models, announced a $305 million Series B to scale its "AI Acceleration Cloud."

2026 Prediction: Open-source AI is poised to capture a significant share of the enterprise AI market, which Gartner forecasts will reach $2 trillion in total spending. Forrester predicts that specialized AI cloud providers ("neoclouds") focused on open-source models will generate $20 billion in revenue in 2026. The choice for enterprises will no longer be between a powerful-but-closed model and a weaker-but-open one.

4. Persistent Memory: The New Moat for AI Applications

Why It's Exploding: Persistent memory has become a critical dual-pronged theme. On the hardware side, technologies like Compute Express Link (CXL) and High-Bandwidth Memory (HBM4) are breaking the "Memory Wall," allowing for the training of multi-terabyte models. On the software side, "long-term memory" systems built on vector databases and knowledge graphs are transforming stateless AI tools into context-aware agents. This software layer is becoming the new competitive "moat," as accumulated intelligence and deep personalization create high switching costs.

Backed by Billions: Investment momentum is strong on both fronts. The CXL memory market is projected to grow from $1.3 billion in 2024 to $12.6 billion by 2033, with giants like Samsung and SK hynix investing heavily. In software, the vector database space has boomed, with Pinecone raising $100 million at a $750 million valuation, and other players like Qdrant, Weaviate, and Zilliz securing substantial funding.

2026 Prediction: On the hardware front, CXL 3.0/3.1 will move into production deployment in major clouds, enabling "memory-as-a-service" offerings. On the software front, breakthroughs in long-term memory will fuel the next wave of breakout social and productivity apps. Expect M&A to increase as incumbents in vertical industries acquire AI memory and agent startups (CB Insights Q1’25).

5. Inference Economics: The New Frontier for Margin Expansion

Why It's Exploding: The AI industry's economic focus is pivoting from the massive, one-off cost of training models to the continuous, exponentially growing cost of inference (using the models). The inference market is projected to grow from $106 billion in 2025 to $255 billion by 2030 (CB Insights Q1’25). This has created a new frontier where the winners will be those who can deliver high-performance AI at the lowest possible cost per token. This trend is fueled by a colossal capital expenditure cycle from hyperscalers, projected to spend nearly $7 trillion on AI-ready data centers by 2030.

Backed by Billions: Investment is pouring into companies specializing in inference. Groq announced a $750 million Series E in September 2025 at a $6.9 billion valuation. The entire ecosystem is being built out at a historic pace, with Google announcing a $40 billion investment in new Texas data centers and Oracle planning to spend nearly $50 billion. Nvidia's Blackwell platform, now in full production, promises up to 25x less cost and energy consumption for inference.

2026 Prediction: The relentless pace of hardware innovation from Nvidia (Rubin platform) and AMD (MI350/400 series), combined with software optimizations, will continue to drive down the cost-per-token. The market will stratify, with specialized Infrastructure-as-a-Service providers (like Groq and Together.ai) competing on pure performance and cost, challenging the dominance of general-purpose clouds.

Contrarian Lens: Middleware Moats Are Replacing Model Moats

While the race for bigger, better foundational models grabs headlines, the real source of defensibility is quietly shifting. The primary value in the AI stack is moving away from the models themselves—which are becoming commoditized—towards the middleware layers that orchestrate, manage, and integrate them into enterprise workflows (Bessemer Venture Partners).

True competitive advantage in 2026 will lie in data governance, agent orchestration, Retrieval-Augmented Generation (RAG), and observability platforms (Bessemer Venture Partners). Evidence from 2025 shows traditional SaaS moats eroding as AI agents automate implementation and data ingestion, lowering switching costs. This is fueling the rise of middleware platforms like Databricks Mosaic AI and Snowflake Cortex (Bessemer Venture Partners). For founders, the message is clear: build deep integrations and specialized agents. For investors, the strategy should shift to backing companies building these indispensable middleware layers.

Investor Heat Map: The Billion-Dollar Club of 2025

The capital fueling these themes is concentrated among a handful of venture firms and corporate strategics. Andreessen Horowitz (a16z) has positioned itself as a premier investor, deploying over $4 billion in 2025 alone (list and analysis).

A compelling visualization for this story would be an annotated timeline or 'lollipop' chart mapping the largest AI funding rounds of $1B+ in 2025 (PitchBook trend report). This visual would chronologically plot deals like OpenAI's record-breaking $40 billion raise and Anthropic's massive $13 billion Series F, with annotations showing the deal value, key investors (like ICONIQ, Fidelity, and Lightspeed), and the associated AI theme (e.g., 'Foundational Models'). This transforms a list of deals into a powerful narrative, showing the accelerating pace and staggering scale of investment into foundational models and AI infrastructure throughout the year.

The Hidden Dynamics: $100M Per Employee Valuations and Systemic Risks

Beneath the surface of these mega-deals are powerful forces shaping the market.

The Talent Premium: Elite AI talent is so scarce that a new valuation metric has emerged: the talent premium. As highlighted in a CB Insights Q3 2025 report, top companies are being valued at up to ~$100 million per employee. For example, humanoid developer Figure was valued at $104.3M per employee, and AI agent creator Cognition was valued at $98.1M per employee. This dynamic fuels "quasi-acquisitions"—complex hiring and licensing deals designed to secure talent—and signals that a company's valuation is increasingly tied to the perceived quality of its team.

The Power Bottleneck: The single biggest long-term constraint on AI's growth is not talent or capital, but electricity. The massive compute required for AI is straining aging grid infrastructure globally. In critical US data center markets like Northern Virginia, interconnection queue wait times for new energy projects have reached up to7 years](https://www.csis.org/analysis/electricity-supply-bottleneck-us-ai-dominance). This is forcing unconventional solutions, like xAI resorting to portable gas-fired generators, and driving a strategic shift toward energy-efficient hardware and massive investment in alternative power sources like nuclear and geothermal energy.

The Final Word: From Experimentation to Execution

As the dust settles on a record-shattering year, the trajectory for 2026 is crystal clear: the age of AI experimentation is giving way to an era of scaled execution. The $216 billion war chest amassed in 2025 is not just funding theories; it's building the engines of our economic future. We're witnessing the dawn of the agentic enterprise, the first steps of humanoid robots in our warehouses, and the democratization of cutting-edge AI through open-source.

The momentum is undeniable. The investments of today are laying the groundwork for a more intelligent, efficient, and automated world tomorrow. The question for businesses and investors in 2026 is no longer 'if' AI will be transformative, but 'how' to be a part of the explosion (PitchBook overview).

The AI investment landscape is moving at light speed, with new deals and breakthroughs announced daily. To stay ahead of the curve and track the money shaping our future in real-time, dive deeper into the data with the Roundly.io AI funding tracker. Follow the capital, watch the trends unfold, and see for yourself which themes are truly ready to explode.

Check out my other blog posts:

Nov 19

Top 20 VCs Investing in AI in 2025 (The Active List)

Nov 15

Top AI Investors 2025 YTD by Dollars and Deal Count

Nov 14

AI Funding Recap Nov 10–14, 2025: $5.02B Across 58 Deals

Nov 13:

Is the AI Bubble 2025 Popping? Decoding Today's $17.3B Mega-Rounds Amid Valuation Red Flags

Nov 11:

Breaking the AI Memory Wall: The $100M Shift from GPU Scarcity to Memory-Centric Computing

Nov 10:

The Geopolitics, Infrastructure, and Commercialization Dynamics of the Global AI Ecosystem

The AI Funding Barbell: What November 10th's $629M Reveals About the New Market